Everything to Know Before Applying: Discover’s personal loans and debt consolidation up to $40,000

We’re going to a quick deep dive into Discover’s personal loans. We’ve spent years working in the lending industry and we track dozens of lenders. We want to break down this lender so you can see whether you would want to use them to consolidate credit card debt, make a big purchase, or use them to cover an unexpected emergency.

But first, a quick note about Discover.

Discover is primarily known as a credit card company. Its cards run on its own network (that is separate from Visa or Mastercard). This is a big company. While 80% of Discover Financial Services revenue comes from their credit card business, they still earn $8 billion a year from personal loans.

Let’s start out by talking about how much you can borrow from them.

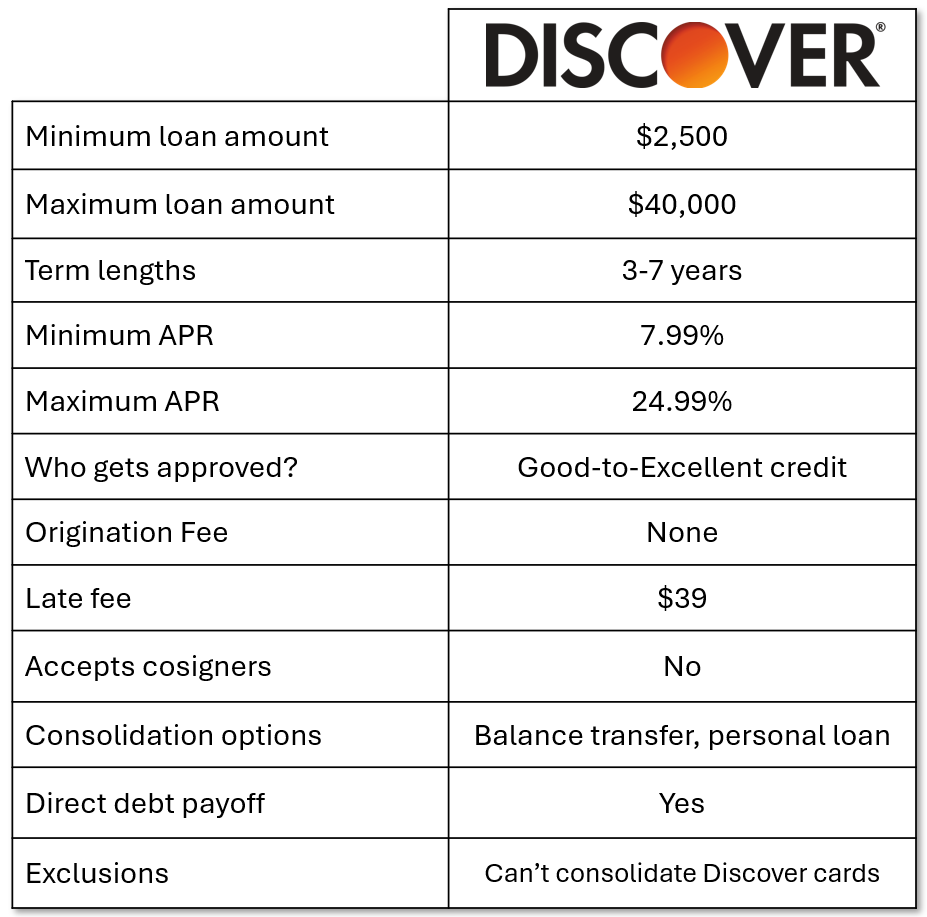

Discover offers a minimum loan amount of $2,500. If you are looking for just a little bit of money to cover a monthly shortfall, there are other lenders that will lend less than $2,000. If you are looking for a more substantial amount of money, Discover will lend as much as $40,000. A pretty standard maximum amount for lenders like Discover is $50,000. So, they are close, but they don’t lend as much as many. Some will offer personal loans as much as $100,000. Still, it’s likely that $40,000 will cover what most people will need.

Discover offers loans with terms between 3 and 7 years.

Seven years is a long time to carry debt, so you will want to be careful not to be enamored by the low monthly payment that comes from a long term. That will keep you paying interest much longer than you should. And, frankly, three years is too long for smaller loans. The good news is that Discover does not charge a prepayment penalty. So you can always shorten your loan term by making extra payments. When you get the loan, sacrifice to make as many extra principal payments in the first year of the loan. That will save you a lot of money on interest and will help you get out of debt faster.

Now let’s look at what the loan costs.

Discover’s minimum APR is 7.99%. 7.99% is one of the lowest in the industry right now, so that’s great. But keep in mind that only about 10% of their borrowers are likely to qualify for their lowest rate. So, it might be more important for you to know that their maximum APR is 24.99%. That’s lower than a lot of lenders, but not as low as some.

That APR range says a lot about the credit score you will need to be approved.

You will almost certainly need a Good-to-Excellent credit score in order to qualify for Discover’s personal loans. Based on my research, I would think you would struggle to be approved if your credit score wasn’t north of 670. But, that’s just a guideline. Most lenders don’t make a decision on credit score alone. They build proprietary algorithms that will also include things like debt-to-income ratio, payment history, type and amount of income, bank transaction data, and other financial data. Your particular mix of these metrics will determine whether you are approved. But, it’s fair to say that Discover will be rather restrictive.

Many lenders will charge an origination fee on their personal loans. Discover will not. An origination fee is a percentage of the borrowed amount, usually between 1 and 10%, that comes out of the proceeds of the loan. The fact that Discover does not charge one means that the full cost of borrowing from Discover is wrapped up in their interest rate. That means you can significantly lower the overall cost of borrowing by paying the loan off early.

If you think you might struggle to get approved for the loan you need, one strategy is to include a cosigner who has a better credit profile than you do. Unfortunately, Discover will not allow you to add a cosigner to their loans. So, if you think you need that option, you will have to find another lender.

If you are late making your payment, Discover will charge you as much as $39. That’s the highest late fee in the personal loan industry. There are a bunch of lenders that don’t charge a late fee at all. Those that do usually charge between $15 and $25. Additionally, Discover doesn’t appear to have a grace period. Many lenders will only charge you if you fail to make the payment within a couple of weeks of your due date. Discover will charge you immediately. So, if you are the type of person who is chronically late with your payments, Discover could end up being more expensive than you bargained for. This is why I would recommend signing up for auto-pay. It’s a great way to make sure you are never late.

Because consolidating credit card balances or other debt is such a common reason for taking a Discover personal loan, I want to spend an extra second talking about their policies for debt consolidation.

Discover boasts about having two different ways of consolidating your credit card debt.

The first one is balance transfer. Balance transfer is where you move your credit card balances onto a Discover credit card. This may feel like just rearranging deck chairs on the Titanic. But, there is one reason why it is worth considering: introductory APRs. If you do open a new Discover card to transfer the balance, they will not charge you interest for 15 months. If you use that time to make aggressive principal payments, it can be a powerful strategy for getting out of debt. If you use it as an excuse to push off addressing your debt, it could just extend the time you are in debt. Also, keep in mind that just because the APR is zero, it doesn’t mean it’s free. There will be a balance transfer fee of 3 to 5% of the amount you transfer.

The second way of consolidating your credit card debt with Discover is through an installment loan. That’s what this whole video is really about: personal loans. Why would you use a personal loan if you could get zero-percent APR by transferring to a new credit card? Personal loans have a fixed payment so you are forced to make more consistent progress paying down the principal. They also have fixed interest rates, so the cost of borrowing won’t adjust based on the Prime Rate. When you consolidate with a personal loan, you also drop your revolving credit utilization which could have a positive effect on your credit score. So, the primary benefits of a personal loan are predictability, consistency, and a definitive end date to your debt.

When you are using the proceeds of the loan to consolidate debt, Discover will use the proceeds of the loan to pay off your other creditors. It’s convenient when a lender will do that, but it’s good for another reason. It shows that the lender understands that the new loan will replace other debts and not stack on top of them. That means that the new loan won’t make your debt-to-income ratio worse. That should make it easier to be approved by them.

When consolidating, Discover does have one key exclusion: they will not use the proceeds of the personal loans to pay off credit card balances from their own company. So, if some of your credit card debt is sitting on a Discover credit card, you will not be able to take out a Discover loan to pay that off. You could get around this a bit if you ask for additional money and pay down the balances yourself. But, then your debt-to-income ratio will not look as good on the application.

What can you use a Discover personal loan for? Because the loan is an unsecured, installment loan, Discover doesn’t limit how you can use the money. Common uses for these types of loans include consolidating debt, financial emergencies, home or auto repairs, moving expenses, wedding expenses, and pet emergencies. I would not use a Discover personal loan for buying a new car, though. You should be able to get a loan with a lower APR with a dedicated auto loan because it will be secured by the title of the motor vehicle.

Let’s summarize Discover’s personal loans.

Discover offers a pretty good range of personal loans, but their terms skew a little longer than I would like. Their interest rates are pretty competitive which is because they lend to people with Good-to-Excellent credit. They do not charge an origination fee, but they have a pretty robust late fee. They won’t allow you to strengthen your application with a cosigner. Finally, they have a couple of different options and features for people who want to consolidate other debt. But, they won’t let you use their loan to consolidate balances on a Discover credit card.

All in all, I think Discover is a pretty good lender. I think you could do a lot worse than taking a personal loan from them. Of course, for many people, the most important thing is whether they can get the money they need at the lowest possible APR. That’s why we always recommend that before you accept a loan, you should shop around. Find the best deal. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions that we didn’t address, leave a comment below and we will try and get it answered. If you found this information useful, please like this video and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card! Whether you need a small amount or $100,000 we have options for you!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!