Everything to know before taking an Avant personal loan. Personal Loan Amounts $2,000 to $35,000.

I’m going to cover everything you need to know about Avant’s personal loans. We’ve spent years working in the lending industry and we track dozens of lenders. I am going to break down Avant so you can make a decision whether you would want to use them to consolidate credit card debt, make a big purchase, or just cover a monthly shortfall.

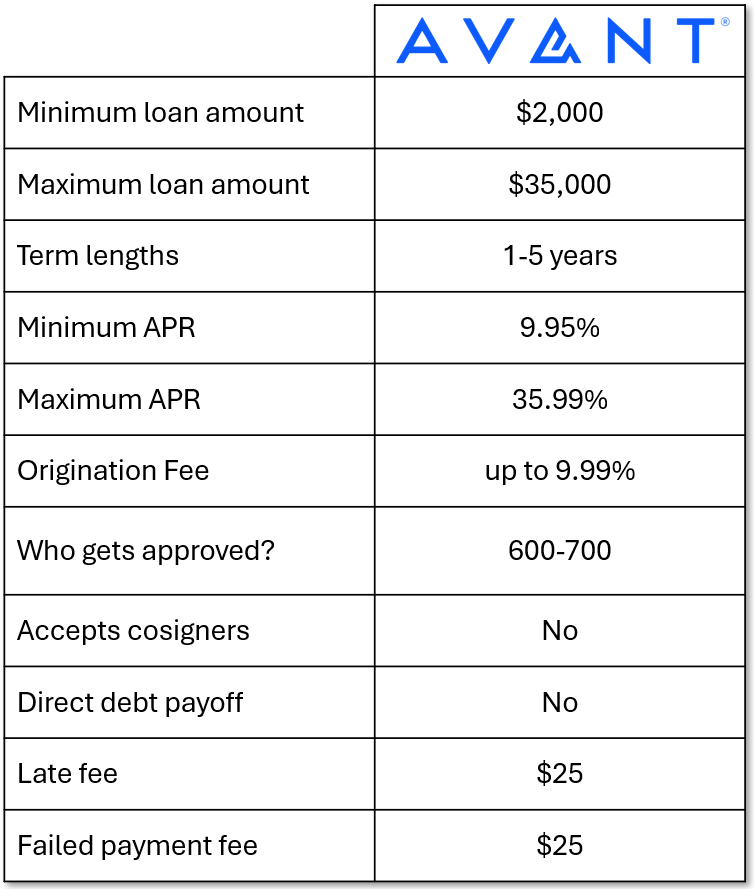

The first question we’re going to answer is how much money can you borrow from Avant.

Avant’s minimum loan amount is $2,000. That might be a little more money than you need if you’re just trying to cover a monthly shortfall. All of these lenders will lend less than that if you just need a small loan. If you are looking for a more substantial amount of money, Avant will lend as much as $35,000. That’s obviously a pretty good amount of money, but these lenders will actually lend up to $50,000.

Loans from Avant have terms between 1 and 5 years.

I like the fact that Avant’s smallest loans have just 1-year terms. Small loans ought to have short terms. Five years is a pretty standard maximum term. If you do end up with a 5-year loan, make as many extra principal payments in the first year as you can. That will save you a lot of money on interest and help you get out of debt faster.

Now, let’s look at the APRs of Avant’s loans.

Their minimum APR is 9.95% and their maximum APR is 35.99%. 36% is a pretty standard APR ceiling. And this a pretty standard range, so it’s not clear what kind of a loan you can get.

Avant charges an origination fee up to 9.99%. Any origination fee above 6% is getting to be on the high side. Although, 10% is still not the highest I’ve seen for personal loans. But it’s important to remember that the origination fee doesn’t increase the overall cost of the loan. The APR includes the origination fee and the interest rate. A loan with a high origination fee but a low APR, is still a low-cost loan. So, should you even care about the origination fee? Yes, especially if you plan on paying the loan off early. When you pay the loan off early, you save money on the interest that you would have paid, but you don’t get a reimbursement of the origination fee. Also, keep in mind that the origination fee will come out of the proceeds of the loan, so you need to borrow enough money to cover your financial emergency as well as the origination fee.

Avant targets borrowers who have Fair credit scores.

I am guessing that they issue loans to people who have credit scores between 600 and 700. Of course, these are just guidelines. Lenders use a lot more than credit score to determine eligibility. They will also look at payment history, debt-to-income ratios, utilization, amount and type of income, and other financial information. A broad mix of these measures will determine the terms of the loan they offer you.

One way to improve your chances of being approved for a personal loan is to include a cosigner. Unfortunately, Avant does not accept cosigners.

If you’re hoping to use the loan to consolidate credit card balances or other debt, some lenders will use the proceeds of the loan to pay off those other creditors directly. Avant will NOT do that. It would be *convenient* if they did, but it’s good for another reason. Doing that shows that the lender knows that the new loan is replacing your other debts and not stacking on top of them. That means it isn’t making your debt-to-income ratio worse. It should be easier to be approved by companies who offer this service.

Avant charges a $25 late fee, which is a rather hefty fee. A few lender in the industry don’t charge a late fee at all. For those that do, $25 is on the high side. If you struggle to make your monthly payments, this isn’t the only fee that you might have to contend with. If you don’t have money in your account when they try to make the ACH withdrawal, they will charge you $25. They call it a “dishonored payment fee.” That fee is also higher than average. So, if you find yourself chronically late on your payments, Avant could end up being much more expensive than you bargained for.

So let’s summarize Avant’s personal loans.

Avant doesn’t have the widest loan amounts in the industry, but they are wide enough to satisfy a lot of people’s borrowing needs. Their APRs aren’t anything special, either. They don’t offer services that other lenders do. And, they have higher fees than others. In general, Avant is pretty middle-of-the-road.

Of course, what could matter the most to you is whether they will offer you the money you need with the best possible terms. Every lender has a different algorithm for approving people. It’s possible Avant could approve you when another lender wouldn’t. That’s why it’s so important that you shop around before you accept an offer. You owe it to yourself to get the best deal you can in your circumstances.

At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions that we didn’t address, leave a comment below and we will try and answer it. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!