Everything to know before taking a Personal Loan Or Debt Consolidation Loan From US Bank

We’re going to give you the rundown on US Bank’s personal loans. We’ve spent years working in the lending industry and we track dozens of lenders. We’ll tell you everything you need to know to decide whether to use them for debt consolidation, a major purchase, or just cover a financial emergency.

US Bank is a retail bank that has locations in 28 states, primarily in the Midwest and West. As a retail bank, US Bank offers a full suite of products. Of course it has checking and savings accounts, but it also offers auto loans, home equity loans, credit cards, and wealth management services. Today, we’ll just be talking about their personal loans, though. Let’s get at it.

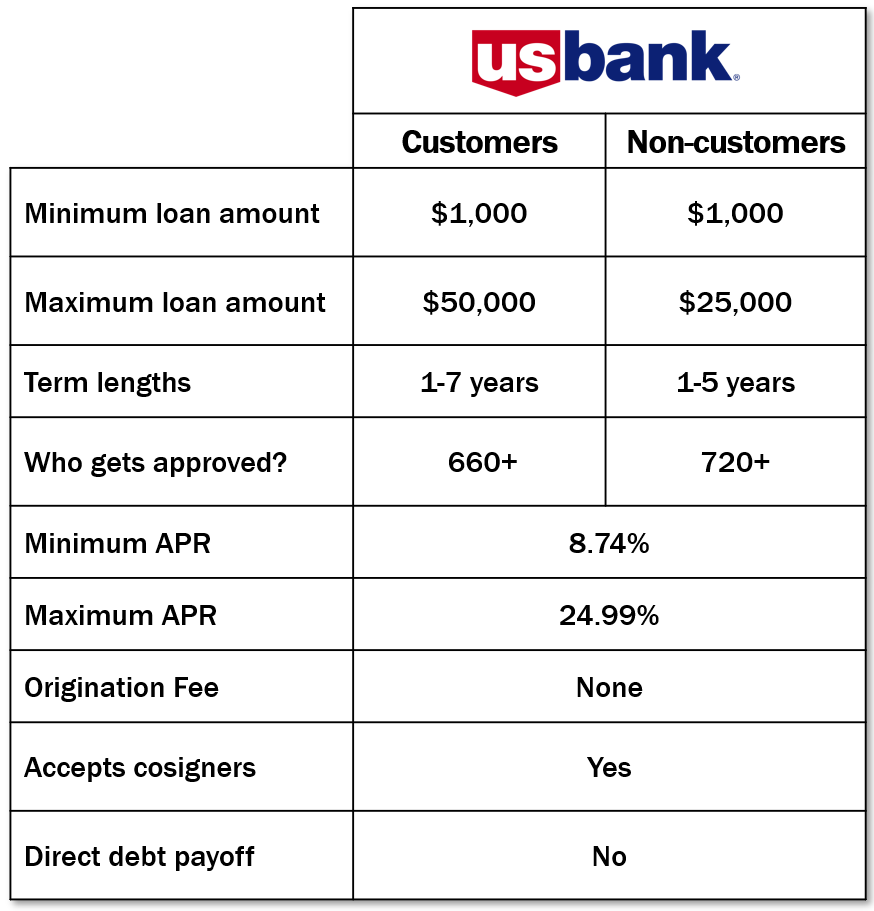

US Bank has different terms for existing customers compared to non-customers. You can qualify for their customer tier of services if you have a US Bank checking account with direct deposit.

Their minimum amount for a personal loan is $1,000.

Not many premium lenders will offer loans that low. That’s great if you just need a little bit of money to cover a monthly shortfall. Separate from their installment loans, they do offer customers what is called a Simple Loan. It is a different kind of product which I won’t cover in this video. Suffice it to say, with a Simple Loan, you can borrow between $100 and $1,000 for three months at a time.

If you are looking for a more substantial amount of money, US Bank will lend customers up to $50,000. That is a very common top amount. There are only a handful of lenders that offer unsecured personal loans for more than that. If you are not a customers, US Bank will not offer you more than $25,000.

For customers, US Bank lends for terms between 1 and 7 years.

If you are borrowing a lot of money, a seven-year term can help keep your monthly payments low, but that will mean paying a lot more interest over time. Because installment loans are amortized, the payments in the first year will carry a lot of interest expense. If you do take a longer term, you should do whatever you can to make extra principal payments in the first year. That will save you a lot of interest in the long run and help you pay the loan off early.

US Bank caps their term lengths for non-customers to 5 years. That’s probably okay, though, since you probably wouldn’t want to borrow $25,000 for a term any longer than that.

The last big distinction between customers and non-customers is in who they approve.

US Bank will approve customers with a credit score above 660. So, this is really only a loan for people with good credit. If you are not a US Bank customer, you will need a credit score above 720. If your credit score is above 720, you probably have a lot of options and should definitely shop around and make sure you are getting the best deal you can.

Now let’s look at the cost of US Bank’s personal loans.

Their minimum APR is 8.74%. Their maximum APR is 24.99%. The APR that they offer you will vary depending on your credit score, loan amount, term length, and purpose of the loan. For instance, you will only qualify for their lowest rate if you borrow at least $10,000, have a credit score of at least 800, and are borrowing for a home improvement project.

US Bank does not charge an origination fee on their loans. In terms of context, I would say about half of all lenders charge an origination fee. It’s great that they don’t charge one; it means that the full cost of the borrowing is wrapped up in the interest rate. That means that the most efficient way to save money on your loan is to make extra principal payments, especially early in the life of your loan.

If you feel like you need to strengthen the quality of your application, US Bank will accept cosigners on their loans. They call them “secondary loan applicants” during the application and a “co-borrowers” during the loan period. A cosigner is someone who agrees to pay off your loan if you fail to repay it. A cosigner is only likely to help your application if they have a stronger credit profile than you do. If you can get the loan that you need on your own, there is no reason to entangle a loved-one in the process.

If you are using the loan to consolidate credit card balances or other debt, US Bank will not use the proceeds of the loan to pay off your other creditors for you. It’s convenient when a lender will do that, but it also shows that the lender understands that the loan will replace other debts and not stack on top of them. Because of that, the new loan won’t change your debt-to-income ratio. That should make it easier to be approved by them.

US Bank has several different options that might meet your credit needs. In addition to personal loans, they also offer home equity loans, home equity lines of credit, and credit cards. If you have a damaged credit history and need just a little bit of money, they offer Simple Loans for under $1,000, but only to customers.

What can you use a personal loan from US Bank for? A US Bank personal loan is unsecured. This means that there are no restrictions on what you can use the money for. Of course, it is generally unwise to borrow money for unnecessary spending, but once you have the money, you can do what you want. Some of the common uses of a personal loan from US Bank include:

Debt and credit card consolidation; Home improvement; Medical bills; Life events like weddings, family planning, and moving; Vacations; and, Emergency expenses.

So, let’s summarize the personal loans from US Bank.

They offer one of the lower minimum loan amounts for a premium lender. So, if you need just a little bit of money they could be a great option for you. If you are looking for a lot more money, they offer more leeway to customers. They have pretty standard term lengths, although 7 years is longer than most. You will need good credit to get approved. And if you are not already a US Bank customer, you will need to be on the top end of “Good” credit to be approved and will likely need Excellent credit. If you need additional support, they will accept consigners on their loans. Their APRs are generally competitive, although there are several premium lenders who have lower top rates. So, you will definitely want to shop around.

After all, one of the most important things about a loan is getting the money that you need at the lowest possible rate. It’s important to remember that each lender will have different criteria for deciding whether to approve you, how much to offer, and at what rate. One of the most efficient ways of shopping around is visiting our marketplace page at The Yukon Project. We’ve tried to make shopping around easy. You can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about US Bank that we didn’t cover, leave a comment below and we’ll try and get it answered. If you found this information useful, please like this video and subscribe to our channel. It helps us continue to make content like this and we really appreciate it. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card! Whether you need a small amount or $100,000 we have options for you!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!