Everything you need to know before taking Upstart personal loans or Upstart Relief Loan!

We’re going to give you a full overview of the personal loans by Upstart so you can decide whether they are the right lender to cover an emergency, consolidate your credit card balances, or make that big purchase.

To understand why they have the policies that they do, it might help to understand something about the company. You see Upstart is a bit unique in the lending industry. Even if you apply for a loan with Upstart, you won’t end up with an Upstart loan. They create the technology that empowers banks and credit unions to lend to customers. They have over 90 banks and credit unions in their network. If you apply with Upstart, you will be getting a loan from one of those companies. But, a lot of that is window dressing. Over 70% of the loans Upstart originates go to their top two lenders.

Now let’s look at the specifics about their personal loans.

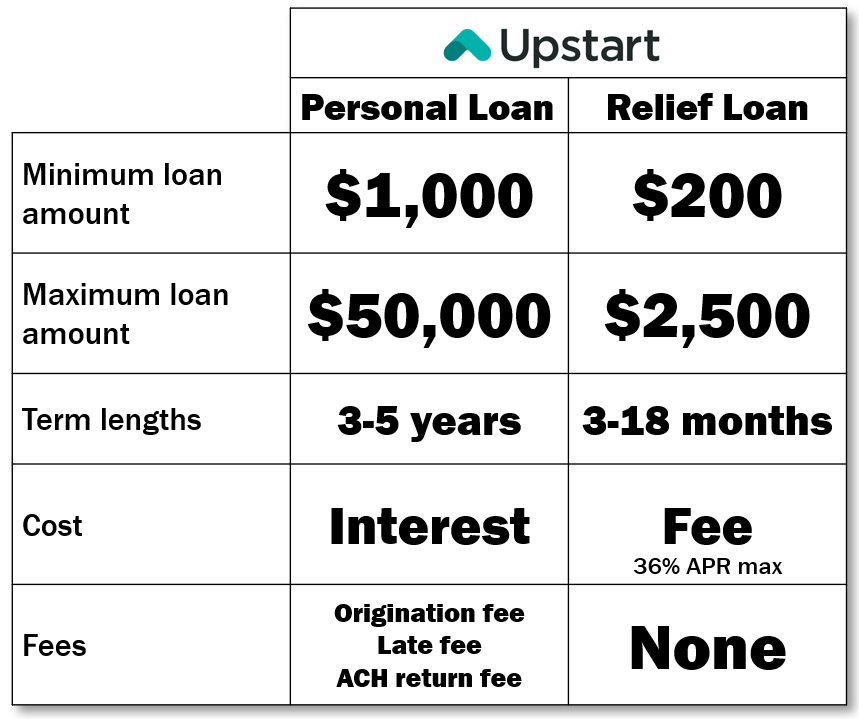

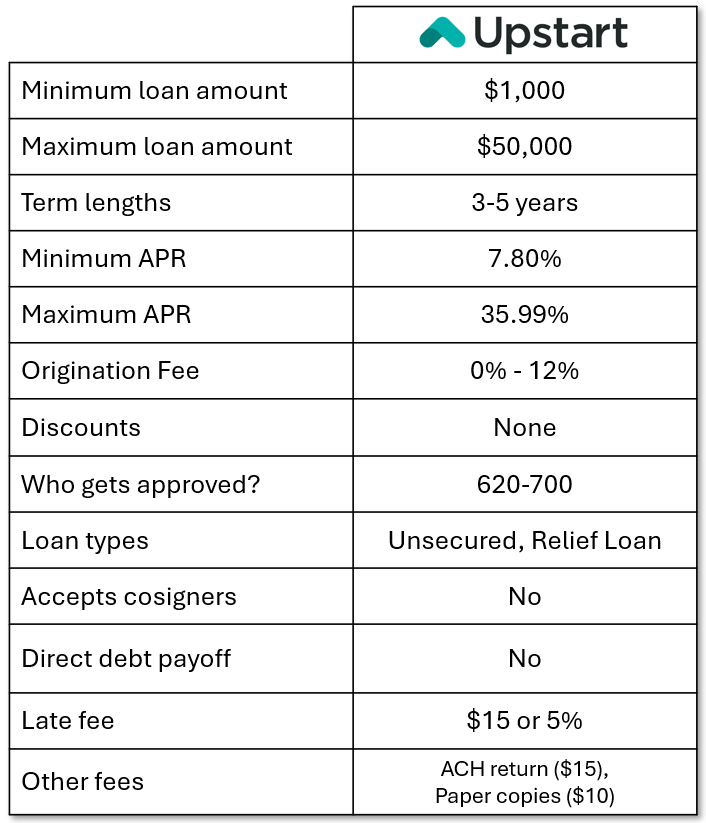

First let’s look at how much you can borrow from Upstart. Their minimum personal loan amount is $1,000. A little later we’ll show you how you might be able to get an even smaller loan through Upstart. So, if you need to cover a small monthly short-fall, Upstart isn’t a bad place to go. If you need a more substantial amount of money, they will lend up to $50,000. That’s enough to consolidate a lot of debt, make a meaningful purchase, or undertake a home renovation.

Loans from Upstart have terms between 3 and 5 years. Five years is pretty standard, but I am a bit concerned about a three year minimum term. If you are only borrowing $1,000, you absolutely do not want to take three years to pay it back. No matter how good your interest rate is. That’s just too long to pay that amount of money back. That will mean paying a lot more interest than you should for what is a small loan.

Now let’s look at the cost of the loans.

Upstart’s minimum APR is 7.80%. 7.8% is one of the lowest minimum APRs in the industry. That is probably being offered by one of their credit union partners. But, don’t get too excited about that rate. I would think less than 10% of their borrowers are able to get a rate that low. Upstart’s maximum APR is 35.99%. There’s nothing particularly special about that maximum. But, it is a little high, especially if you are borrowing a substantial amount of money.

Upstart has one of the broadest ranges for origination fees in the industry. Their fees range from 0% all the way up to 12%. That broad range might be because of the many lending partners that they have. Obviously, zero is a great number. But 12% is about as high as anything in the industry. If you have a low APR and a high origination fee, you are still getting a good rate. Remember that the origination fee is accounted for in the APR. The APR is the origination fee plus the interest rate. So, should you care what the origination fee is? Yes, especially if you are planning on paying the loan off early. Paying early will save you money on the interest you would have had to pay, but you don’t save money on the origination fee.

Upstart offers loans to people who have fair-to-good credit scores.

I would think you have a chance of approval if you have a credit score between 620 and 700. Lately, Upstart has been more restrictive than usual for business reasons, so don’t be surprised if you are squarely in that range and still can’t get approved. But shopping around for the best deal is always a good idea anyway.

Upstart offers unsecured personal loans. Their website looks like they offer loans for moving, weddings, medical bills, and home improvement. But it’s all the same loan. The distinction is really just marketing. They are talking about launching a home equity loan, but it’s unclear when—or if—it will come out. They do offer something that’s called a “Relief Loan.” And if you are looking or just a little bit of money for a short term loan, this could be a good option for you.

The Relief Loan is a bit different than their traditional personal loan. The Relief Loan ranges from $200 to $2,500 with a term between 3-18 months. So, these are really designed for small-dollar, short-term emergencies. They are best for just getting you over a small financial hump. The cost of this loan is a bit different too. While the personal loan charges interest, the Relief Loan charges a fee. The fee won’t exceed a 36% APR. The Relief Loan doesn’t have origination fees or late fees. So, the Upstart Relief Loan would be a much better option than turning to a payday loan. The question is whether a Relief Loan would be better than an Upstart personal loan if you are just looking $2,000. That will definitely depend on the terms you’re offered. It’s possible that the personal loan would have a lower APR.

If you would like to use an Upstart loan to consolidate credit card balances or other debt, you need to know that Upstart will not directly pay off your other creditors for you. Some companies will do that. And it’s convenient, but it’s important for another reason. When a company pays off your creditors for you using the proceeds of the loan, they are taking into account that the new loan will replace those other debts and not stack on top of them. That means they understand that the loan will not make your debt-to-income ratio worse. Consequently, it should be easier to be approved by them.

Does that mean that using Upstart to consolidate your other debt would be a bad idea? Not necessarily. If Upstart will offer you a loan with and APR that is 2-3 percentage points lower than the interest rate on the debt you want to consolidate, it would probably be worthwhile.

If you are late on a payment, Upstart will charge either $15 or 5% of the late amount, whichever is greater. Most lenders will charge a late fee and that’s a fairly standard rate. You won’t get hit with the fee immediately though. Upstart will give you 15 days past your due date to make the payment before they hit you with the fee.

But a late fee is not the only fee that Upstart will charge. They charge a $15 ACH return fee. If your check bounces or they can’t withdraw your payment using ACH, they will hit you with the fee. So, just because you aren’t 15 days late, you could still get hit with the failed payment fee. They will also charge you a one-time fee if you don’t want to eSign for your loan agreement. If they need to send you a paper copy of your loan agreement, they’ll charge you $10.

What can you use an Upstart loan for?

Well really…anything. As a personal loan, they don’t put any restrictions on how you can use the funds. The most common uses of an Upstart loan include:

- Life events such as weddings and moving

- Emergencies like auto repair, medical expenses, and monthly shortfalls

- Large purchases like home improvement

- And consolidating debt or credit card balances

So what conclusions can we draw about Upstart?

I think the most challenging thing about an Upstart personal loan is not being sure of what you can get. Because they work with other lenders, their ranges are pretty broad. Are you going to get a low APR or a high one? Will they offer you a loan with no origination fee or a high origination fee? They also don’t have the customer-centric features that you might expect. And while they do have fees, they are generally not exorbitant. I think Upstart is a pretty decent lender, but unless you are getting the money that you need for the lowest possible APR, there’s no reason not to keep looking. That’s why we always recommend that before you accept a loan, you should shop around. Find the best deal. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about Upstart or their loans, leave a comment below and we will try and answer it. If you found this information useful, please like this video and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!