Spotloan Personal Loan review: How it works & what it costs. Great for poor credit up to $800.

If you have poor credit and you’re in need of a little bit of money to cover a short-term emergency, you might have come across SpotLoan. We are going to talk about who they are, what their loans are like, and whether you should use them. We’ve spent years in the lending industry and we track nearly a hundred lenders. We’ll tell you what you need to know in order to decide whether you want to borrow from SpotLoan.

Summary of loans from Spotloan

SpotLoan only lends small amounts of money for short terms. They will lend between $300 and $800 with terms up to 11 months. When you apply, you will be able to choose the amount you want to borrow, how long you want the loan to last, and whether you want to make payments every other week or monthly.

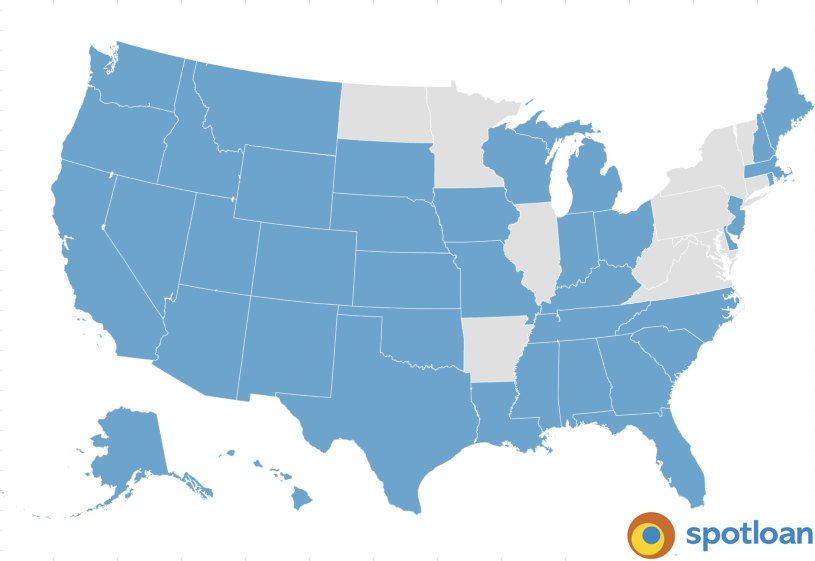

Where does Spotloan lend?

SpotLoan lends in most US states. If you live in any of these states you would be able to apply for one of their loans online. They do not lend in 11 states.

Who qualifies for Spotloan?

These loans are for people who have poor or bad credit and struggle to get money through traditional lending. You need to have a job or other regular source of income, a checking or savings account, can verify your identity, and be at least 18 years old. While SpotLoan will not check your traditional credit report, they will use alternate credit reporting agencies such as DataX and Clarity to determine whether to extend you credit.

Should you use Spotloan?

These are expensive loans. The first time you take out one of their loans, the APR will be 490%. If you take a second loan, you could be eligible for a lower rate of between 330% to 460%. On your tenth SpotLoan, you could earn an APR as low as 99% and borrow as much as $1,500. SpotLoan will not charge a late fee if you miss a payment, but they will continue to charge you interest, which would be more than a late fee, anyway. However, if they attempt to take a payment from your bank account using an ACH draw and you don’t have enough money in the account, they will charge you a $10 NSF fee.

Why is Spotloan APRs so high?

The APR is indeed 490%. You might be asking yourself whether that interest rate is legal or not. In fact, you may live in a state where that interest rate exceeds the state usury cap.

So, how do they do it?

Well, SpotLoans is owned by a company called BlueChip Financial, which is owned and operated by the Turtle Mountain Band of Chippewa Indians in North Dakota. Because they are a federally recognized tribe, they claim sovereignty. This legal doctrine grants the tribe a degree of autonomy and self-governance, which can exempt them from certain state and federal regulations.

It’s the same principle that has allowed tribes to open casinos in states where gambling is illegal. SpotLoan makes a point of claiming that you are digitally “visiting” their reservation when you apply for a loan from them and therefore are subject to their jurisdiction.

Examples of Spotloan

490% APR is hard to wrap your brain around. So, let me show you what it would look like.

11 month Spotloan

If you borrow $500 for 11 months at a 490% APR, you will end up paying $2,089 back. That’s $1,589 in interest alone. Because these loans are amortized, the first several months of payments look like all you are doing is paying interest…and that’s not far from the truth. You first bi-weekly payment of $87.63 comprises of only $2.03 going to principal.

| Beginning Balance | Interest | Principal | Ending Balance | |

| 1 | $500.00 | $85.60 | $2.03 | $497.97 |

| 2 | $497.97 | $85.26 | $2.37 | $495.60 |

| 3 | $495.60 | $84.85 | $2.78 | $492.82 |

| 4 | $492.82 | $84.37 | $3.26 | $489.56 |

| 5 | $489.56 | $83.82 | $3.81 | $485.75 |

| 6 | $485.75 | $83.16 | $4.47 | $481.28 |

| 7 | $481.28 | $82.40 | $5.23 | $476.05 |

| 8 | $476.05 | $81.50 | $6.13 | $469.92 |

| 9 | $469.92 | $80.45 | $7.18 | $462.74 |

| 10 | $462.74 | $79.22 | $8.41 | $454.34 |

| 11 | $454.34 | $77.78 | $9.85 | $444.49 |

| 12 | $444.49 | $76.10 | $11.53 | $432.96 |

| 13 | $432.96 | $74.13 | $13.50 | $419.45 |

| 14 | $419.45 | $71.81 | $15.82 | $403.64 |

| 15 | $403.64 | $69.11 | $18.53 | $385.11 |

| 16 | $385.11 | $65.93 | $21.70 | $363.42 |

| 17 | $363.42 | $62.22 | $25.41 | $338.00 |

| 18 | $338.00 | $57.87 | $29.76 | $308.24 |

| 19 | $308.24 | $52.77 | $34.86 | $273.39 |

| 20 | $273.39 | $46.81 | $40.82 | $232.56 |

| 21 | $232.56 | $39.82 | $47.81 | $184.75 |

| 22 | $184.75 | $31.63 | $56.00 | $128.75 |

| 23 | $128.75 | $22.04 | $65.59 | $63.16 |

| 24 (Partial) | $63.16 | $10.81 | $63.16 | $0.00 |

3 month Spotloan

If you borrow that same $500, but decide that you only want the loan to last for three months, you end up repaying $866.70, with $366.70 of that going to interest. In this case, your first bi-weekly payment of $133.34 has $47.74 going to principal.

| Beginning Balance | Interest | Principal | Ending Balance | |

| 1 | $500.00 | $85.60 | $47.74 | $452.26 |

| 2 | $452.26 | $77.43 | $55.91 | $396.36 |

| 3 | $396.36 | $67.86 | $65.48 | $330.88 |

| 4 | $330.88 | $56.65 | $76.69 | $254.19 |

| 5 | $254.19 | $43.52 | $89.82 | $164.37 |

| 6 | $164.37 | $28.14 | $105.20 | $59.17 |

| 7 (Partial) | $59.17 | $10.13 | $59.17 | $0.00 |

1 month Spotloan

One more scenario. Let’s say you only need the $500 for a single month. In this case you will be repaying $639.69 with $139.69 in interest. In this case, you only make two full payments and a partial payment. Your first payment of $295.24 will have $209.64 going towards principal.

| Beginning Balance | Interest | Principal | Ending Balance | |

|---|---|---|---|---|

| 1 | $500.00 | $85.60 | $209.64 | $290.36 |

| 2 | $290.36 | $49.71 | $245.53 | $44.83 |

| 3 (Partial) | $44.83 | $7.67 | $44.83 | $0.00 |

So, as you can see. These are expensive forms of credit, and they are really only viable if you are borrowing for a very, very short period of time. If you hold these loans for even a few months, they can get out of hand. If you didn’t have $500 initially, paying back $2,000 can’t be very easy.

Where to shop around

If you want to see whether you could qualify for a better loan than this, visit our marketplace page at The Yukon Project. You can select the loan amount you need and even indicate what your credit score is. When you apply to one of our featured lenders, we will check your rate with up to 40 other lenders behind the scenes. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all the offers you can qualify for, so you can have more confidence about what you should be paying for credit.

Conclusion

If you struggle to get approved for a personal loan because you have poor or bad credit, Spotloans would probably approve you. However, these loans have very high APRs so you will only want to take one of these loans if you know you can pay it back within six weeks.