11 Facts Before Getting A PENFED Personal Loan or a HAPPY MONEY Personal Loan. UNSECURED LOANS.

We’re going to compare personal loans from Penfed and Happy Money. We’ve spent years working in the lending industry and we track dozens of lenders. We want to break down these two lender so you can see which one might be better for your situation.

First, a quick comment about these two companies. Penfed is a credit union that was originally formed for the employees of the armed forces and federal government, but they have long since opened their charter so that anyone may join. Happy Money is a financial services company that connects people looking for personal loans with credit unions. Traditionally, credit unions often have cheaper APRs than banks or consumer finance companies. But, they can also be a bit restrictive, especially if you are not already a member. So, let’s see what these how these two organizations compare.

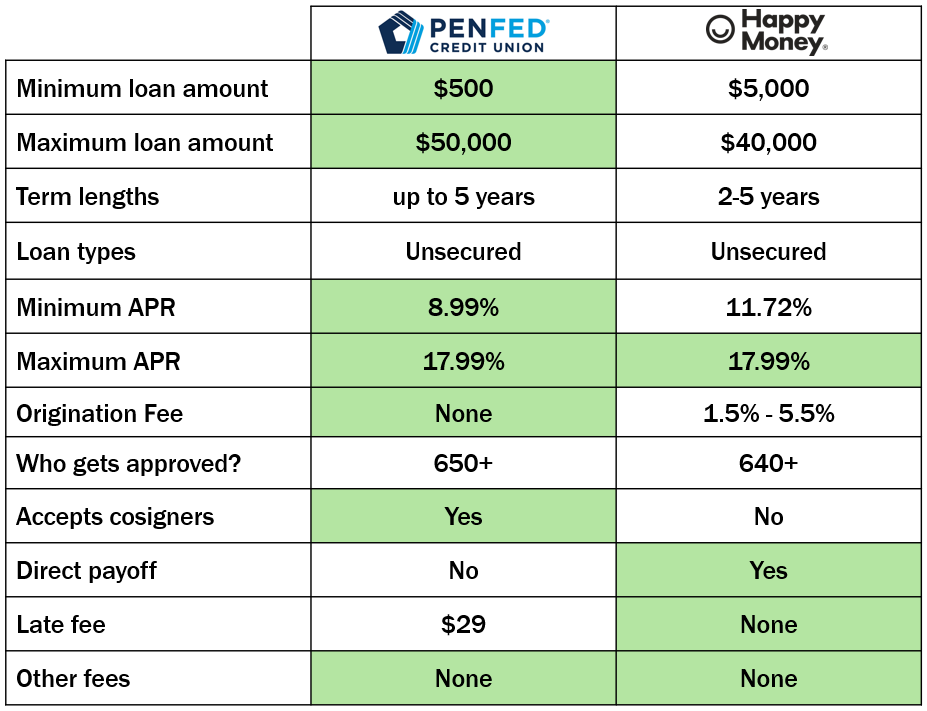

First, let’s look at the loan amounts that they offer. Penfed’s minimum loan amount is only $500. This is actually quite unusual. Few institutions will lend only a few hundred dollars because it is so challenging to cover their overhead with such limited interest earned. Happy Money, on the other hand, will not lend less than $5,000. So, they definitely aren’t the place you want to go if you have a monthly shortfall or a minor emergency. Penfed gets credit for flexibility on the low side.

If you are looking for a more substantial amount of money, Penfed will lend up to $50,000 and Happy Money will lend as much as $40,000. Penfed gets the credit for the higher loan amount. For both of these lenders, it’s important to remember that the amount that they offer you will depend on your particular financial situation.

Penfed personal loans have terms that go up to 5 years. While Happy Money lends between 2 and 5 years. Neither lender will charge a prepayment penalty, so it’s always a good idea to pay the loan off early. The way to save the most money on interest is to make as many extra principal payments in the first year of the loan.

Both Penfed and Happy Money only offer unsecured loans, which means that you don’t have to put up any collateral—like the title to your motor vehicle—to secure the loan. This also means that if you struggle to repay the loan, they can’t seize any of your assets as repayment. I generally think it’s a good idea for personal loans to be unsecured. However, securing a loan can make it easier to be approved, or to get a better rate than you otherwise would. Still, neither of these lenders offer secured loans.

Now let’s look the cost of the loans. Penfed’s minimum APR is 8.99% and Happy Money’s minimum is 11.72%. Penfed gets credit for having the lower APR. Both of them have maximum APRs that cap out at 17.99%. That is a really good top APR. There are very few lenders who match that. So, I am going to highlight both of them.

Penfed does not charge an origination fee at all. Happy Money will charge between 1.5% and 5.5%. Happy Money’s origination fees are actually pretty good, but zero is still lower, so Penfed gets highlighted. The origination fee is a percentage of the borrowed amount and comes out of the proceeds of the loan. So, if you borrow $10,000 and have a 5% origination fee, you will receive $9,500 but will still need to repay the $10,000. Remember that the origination fee is accounted for in the APR. The APR is the origination fee plus the interest rate. All things being equal, you want a lower origination fee if you plan on paying off your loan early. Paying off early will save you on the interest you would have paid, but you don’t get a reimbursement of the origination fee.

Both Penfed and Happy Money target borrowers who have good to excellent credit. Based on my research, I believe Penfed only lends to people with credit scores of 650 or above and Happy Money lends to people with credit scores of 640 and above. Of course, the lower you go down in their ranges, the less likely you are to be approved. But, these are only guidelines. Lenders don’t usually use credit score to determine eligibility. They usually use information like payment history, debt-to-income ratios, utilization, income…stuff like that. It makes sense that these two lenders would be rather stringent because of their low top APR.

Penfed will accept a cosigner on their loans, but Happy Money does not. A cosigner is someone who agrees to pay off your loan if you fail to repay it. If you can qualify for the loan that you need, there is little reason to entangle a loved one in the process. But, if you have a spouse or loved one that has a stronger credit profile than you do, add them as a cosigner might make all the difference in getting the loan you need. It’s good that Penfed offers this option.

If you are using the loan to consolidate credit card balances or other debt, Happy Money will directly pay off those other creditors with the proceeds of the loan for you. Penfed, on the other hand, will not. It’s convenient when a lender will do that, but it also shows that the lender knows that the loan will replace other debts and not stack on top of them. Because of that, the new loan won’t change your debt-to-income ratio. That should make it easier to be approved by them. I think its great that Happy Money offers this service.

Happy Money does not charge a fee if you are late with your monthly payment, but Penfed will charge $29. While $29 is not the highest late fee in the industry, it is certainly higher than average. So, Happy Money gets credit for not having a fee at all.

Some lenders will charge bounced check fees, paper documents fees, and other fees. Neither of these lenders will charge other fees, which is great.

So, let’s summarize what we’ve learned about personal loans offered by Penfed and Happy Money.

Penfed clearly wins more of the categories, but Happy Money does pretty well. I really don’t think you can go wrong with either one of these lenders. But, they each have different reasons for using them. If you need just a little bit of money, Penfed is better. If you are trying to consolidate your debt, Happy Money would probably be better. If you need a cosigner’s help to get the money you need, Penfed will be better for you. If you have been late on payments in the past, Happy Money might be better. Really, though, the most important things for people looking for a loan are whether they can get the money they need and whether they can get it at the lowest possible price.

That’s why we always recommend that before you accept a loan, you should shop around. Find the best deal. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about either one of these lenders that we didn’t cover, leave a comment below and we will try and answer it. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!