Everything you need to know about NetCredit Personal Loans. Is it right for you? $500 to $10,000 Personal Loan.

I want to tell you everything you need to know about NetCredit personal loans. I want you to have the information to know what the loans are good for, how much they cost, and any of the hidden policies that could sneak up on you. Let’s do it!

First thing we’re going to look at are the loan amounts that they offer.

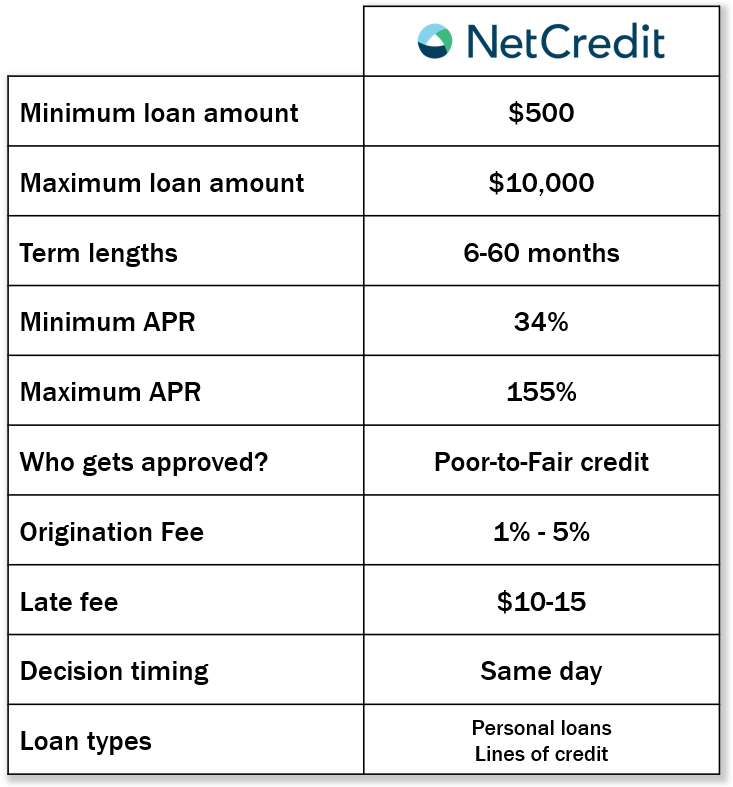

After all, if they don’t give you the money that you need, there’s not much point in considering them. The minimum loan amount seems like a simple enough idea, but many of NetCredit’s policies are state-specific. And what minimum loan amount they offer is one of them. They lend as little as $500, but only in 8 states. In another 20 states, the minimum is $1,000. In the remaining 8 states where they offer loans, the minimum is higher than a $1,000. So, if you need just a little bit of money, NetCredit might be a good alternative to payday loans…depending on which state you live in, of course.

NetCredit will lend as much as $10,000 in all of their states.

NetCredit offers loans as short as 6-months…but only in a third of their states. In two-thirds of the states, the minimum loan term is 12 months. In all but one of their states, the maximum term length is 60 months, or 5 years. Honestly, 5 years seems like a long time to be paying back a loan that is less than $10,000. You do not want to carry a NetCredit loan for 5 years. The good news is that NetCredit does not charge a prepayment penalty, so you can be aggressive in paying it off early. Extra principal payments in the first six months of the loan will be 2 or 3 times as valuable as extra principal payments at the end of the loan. If you make extra payments early, you will save a lot of money on interest and get out of debt faster.

Now let’s look at the cost of a NetCredit personal loan.

NetCredit’s minimum APR is 34%. Their maximum APR is–you guessed it–dependent on the state in which you live. The most common maximum APR is 100%. You can see that is offered in 22 of the states. For eight states, the maximum is 155%. For the remaining six states the maximum APR is between 36% and 59%.

The reason for the APR being so high is found in who they approve. They lend to people who have poor-to-fair credit. I believe that most of their borrowers have credit scores between 550 and 650. People with poor credit don’t have many options, so it’s not uncommon for them to default on loans if they run into additional trouble. Of course, most borrowers pay back without any trouble. But NetCredit does have to write off about 15% of the money they lend out. They charge a higher APR to compensate for those losses.

You do need to be aware of NetCredit’s billing cycle.

Most people just assume that their payment will be monthly. But, for NetCredit, you may need to make payments bi-weekly, semi-monthly, or monthly. The length of your billing cycle depends on how often you receive income. NetCredit lines up your payment schedule with the days you are paid. So, if you are paid every other week, your billing cycle will be bi-weekly. If you are paid twice a month, your schedule will be semi-monthly. You need to be aware of this when you receive your loan offer. You don’t want to think that the payment is monthly only to find that you are paying that amount twice a month.

NetCredit offers two types of personal loans.

The first type is a personal loan. These are unsecured, installment loans. You don’t need any collateral to qualify. This is good because it means that they can’t come after your motor vehicle, your home, or any other assets if you struggle to repay the loan. On these installment loans, the payment is fixed as well. So, your first payment will be the exact same amount as your last payment.

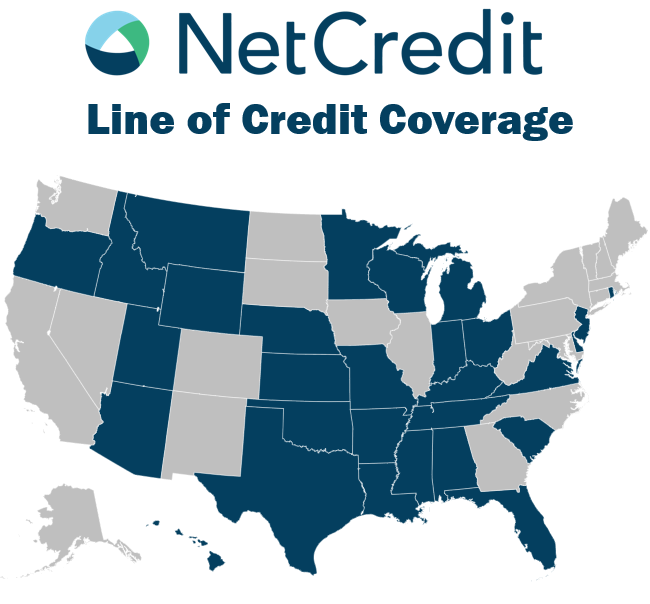

The other type of credit that they offer is a line of credit.

A line of credit gives the borrower access to a certain amount of funds and can draw on and pay down as they need. Some people love this flexibility. Others don’t like how easy it is to stay in debt. I need to do a whole other video on NetCredit’s lines of credit because they have a very different structure and fees. If you are interested in me covering them, leave a comment below. For this video, though, I’m going to stick with their personal loans.

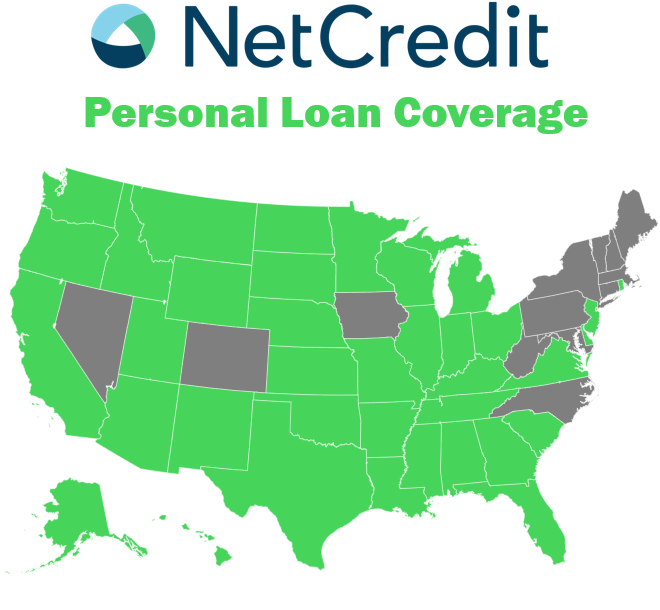

NetCredit offers personal loans in 37 states.

You can see that they largely stay out of the Atlantic northeast. Of course, this doesn’t tell the whole story. Remember, that many of their policies are state-specific. So, you will want to check your state for the amount, term length, and maximum APR. They don’t offer their line of credit in as many states. You will only be able to get a line of credit through NetCredit if you live in one of these states.

NetCredit will make a decision on whether to lend you money on the day that you complete and submit your application. In fact, their systems are automated. You are likely to know within minutes whether they approve you and for how much. Likewise, they say that you can have the money in your account as soon as the next business day. So, if your emergency is time-sensitive, NetCredit could get you the money you need quickly.

Now let’s look at the fees that NetCredit charges.

NetCredit charges an origination fee between 1% and 5%. An origination fee comes out of the proceeds of the loan. For example, if you borrow $2,000 and have a 5% origination fee, you will actually only receive $1,900. Of course, you will still need to pay back the $2,000. If you are borrowing money for a specific need, remember that you need to borrow enough to cover the origination fee. The other thing I will say about the origination fee is that it is accounted for in the APR. The APR is the origination fee plus the interest rate.

NetCredit will charge you a $10-15 late fee if you fail to make all or any part of your scheduled payment within 10 days of the due date. Even the late fee policy varies by state, though, so make sure you understand what it will be for you. You don’t want to be hit with surprises in the middle of your loan. NetCredit will not charge any NSF fees. NSF stands for “non-sufficient funds.” Some lenders will charge you a fee if they attempt to draw your payment and you don’t have enough money in your account to cover it. It does seem to be a cruel joke to charge a customer for not having the money to pay you. If they don’t have the money to pay you, they don’t have the money for the fee. Fortunately, NetCredit doesn’t charge NSF fees.

How can you use a NetCredit personal loan?

In reality, you can probably use the money for anything you want, because they don’t put any stipulations on how you can use the funds. But, the size and cost of these loans gives us a clue as to the best uses of the money. If you need a little bit of money to cover a monthly short-fall or to cover a small emergency, NetCredit is probably a good option. NetCredit loans are too expensive to use them to consolidate other debt or credit card balances. And I think they are definitely too expensive for discretionary spending, like vacations. Ideally, you never go into debt for a vacation. But, if you do, a good rule of thumb is to never borrow more than you can pay back before you want to take your next vacation.

So, let’s summarize NetCredit Personal Loans.

NetCredit offers loans to people with Poor-to-Fair credit. And because of that, their personal loans tend to be an expensive form of credit. But, the loan amounts are low enough that they are definitely a cheaper alternative to payday loans. They are probably best to cover a short-term emergency that you can easily repay quickly. You probably will not want to borrow a more substantial amount of money because it will be very expensive if it takes years to repay.

If you have poor or damaged credit, you might feel like you don’t have many options. The most important thing you can do is to shop around. Make sure you are getting the best deal you can possibly get in your situation. Remember that every lender has a different algorithm. You might be rejected by one only to be accepted with better terms from a different lender. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our featured lenders and behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about NetCredit, leave a comment below and we will try and get it answered. If you found this information useful, please like this video and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!