Navy Federal Credit Union Personal Loan vs USAA Personal Loan: Who’s got the best personal loan?

We’re going to compare the personal loans offered by Navy Federal Credit Union and USAA. We have spent years in the lending industry and track dozens of lenders. We are going to bring that experience to help you make the decisions that would be best for your personal finances.

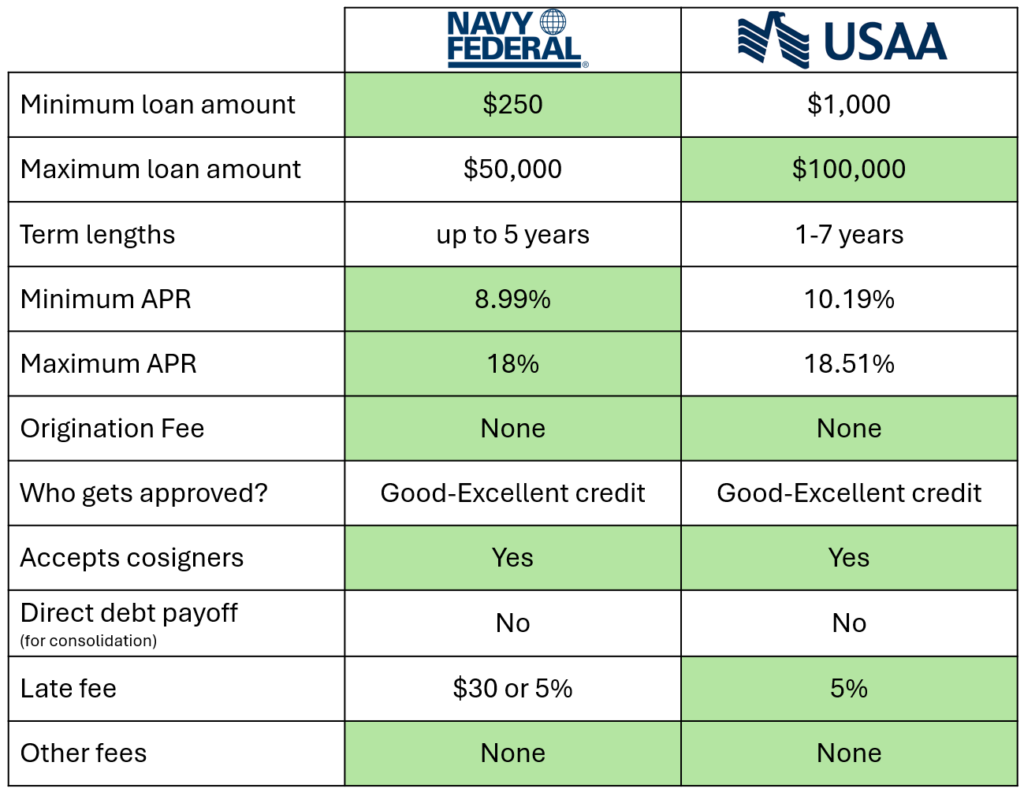

The first thing we are going to look at is the personal loan amounts that they offer.

Navy Federal Credit Union offers micro personal loans to its members. The lowest amount they offer is $250. USAA’s lowest amount is $1,000. So, if you are looking for just a little bit of money to cover an emergency, either company is a good choice, but Navy Federal offers more flexibility. On the other hand, if you are looking for a substantial amount of money, Navy Federal will lend up to $50,000, which seems like a lot of money to me, but USAA will lend up to $100,000. USAA gets the marks on maximum loan amount.

Navy Federal’s personal loans have terms that go up to 5 years while USAA’s personal loan terms are between 1 and 7 years. Seven years is a long time to carry a loan, but if you are borrowing as much as $100,000, you probably need a term that long. Neither one of these companies charge a prepayment penalty, so you should definitely work to pay the loan off early. If you have a longer term, making extra principal payments in the first year of the loan will save you a lot of money on interest over the life of the loan.

Now let’s look at the cost of the two personal loans.

Navy Federal’s bottom APR rate is 8.99% and USAA’s is 10.19%. Navy Federal gets the credit for having the lower rate, here. Navy Federal’s maximum APR is 18%. USAA’s maximum tops out at 18.51%. That difference is hardly worth mentioning, but better is better, so Navy Federal gets highlighted.

Now let’s look at their origination fees. Neither Navy Federal nor USAA charge an origination fee.

When it comes to who the two companies approve, they both target people who have Good-to-Excellent credit. What is unique about both of these companies is that they cater to people who are in the military or Department of Defense. They take this mission very seriously. So, if you are a long-time member in good standing, it is possible that they would approve you even if your credit is not pristine.

Now let’s compare the features between Navy Federal Credit Union Personal Loan vs. USAA Personal Loan.

The first thing we are going to look at is whether they accept a cosigner. Both Navy Federal and USAA accept cosigners on their loans. A cosigner is someone attached to the loan who will agree to pay it off if you fail to. So, it can be risky for someone to act as a cosigner. If your credit situation isn’t good enough to be approved for the loan you need, a cosigner can help. If that person has a stronger credit history, add them to the loan could make all the difference between being accepted or rejected.

Neither companies will directly payoff your other debts if you use their loan to consolidate other debt. I think that is a bit of a problem. It is convenient when a lender offers this service. But it’s important for another reason. Companies who will directly pay off your debts for you know that the money they are lending you will be used to pay off other debts and not stack on top of them. By sending the money directly to those other creditors, it also means that they KNOW you will use the money that way. You are more likely to be approved because the new loan isn’t fundamentally changing your debt-to-income ratio. Unfortunately, neither of these companies will do it.

Next, late fees. Navy Federal charges $30 or 5% of the late amount, whichever is higher. $30 is a pretty high late fee, so you want to be aware of that. USAA charges 5% of the late amount. USAA wins this category because 5% will be lower than $30 in many cases.

Some companies charge other fees as well. Fees like NSF fees, bounced check fees, paper check fees…stuff like that. Neither one of these companies charges any of these other fees.

Okay, let’s summarize everything between a Navy Federal Credit Union Personal Loan vs. USAA Personal Loan.

Navy Federal and USAA are pretty evenly matched. Either one of these companies would be good options for a personal loan.

Of course, for many people, the most important two things are whether they can get the money they need and whether they can get it at the lowest possible price. That’s why we always recommend that before you accept a loan, you should shop around. Find the best deal. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our featured lenders and behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you do end up with a personal loan from Navy Federal or USAA, come back and leave a comment about how it went. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!