10 Things To Know About LightStream Personal Loans & Discover Personal Loans Before Choosing One!

We’re going to compare personal loans from LightStream and Discover. We’ve spent years working in the lending industry and we track dozens of lenders. We want to break down these two lender so you can see which one might be better for your situation.

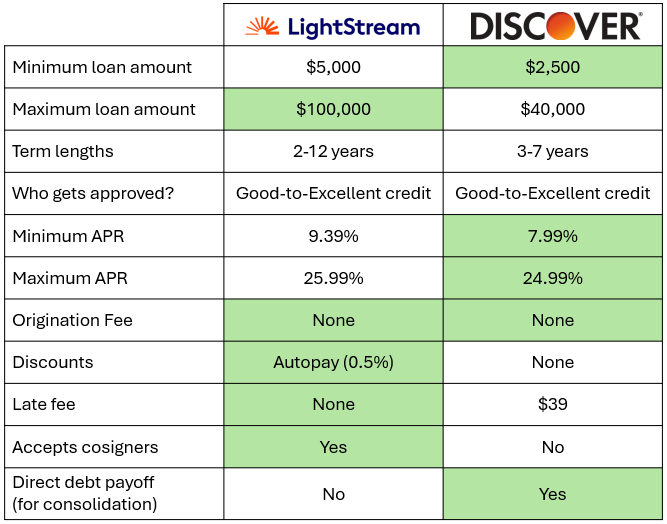

The first thing we are going to look at is the loan amounts that they offer. LightStream’s lowest loan amount is $5,000, so they are not going to be your first choice if you have a small emergency. Discover offers loans as low as $2,500. They may be a great option to cover a short-term gap. If you are looking for a more substantial amount of money, LightStream will lend as much a $100,000 while Discover caps out at $40,000. So, LightStream wins on the higher end.

LightStream’s terms range from 2 to 12 years. Twelve years is the longest term I have seen from the lenders we track. That is a long time to be in debt. If you can avoid it, you don’t want to be paying interest that long. Discover lends between 3 and 7 years. Three years seems too long for small loans and seven years seems too long for the average Discover loan. If you go with either of these companies, you should actively structure the term length you want rather than just accept what they offer you.

Both LightStream and Discover appear to cater to people with Good-to-Excellent credit. The minimum credit score for these loans is likely 660. But, that’s just a guideline. It will entirely depend on your credit profile and financial situation.

Now let’s look at the cost of the two loans. LightStream’s lowest APR is 9.39% and Discover’s is 7.99%. 7.49% is one of the lowest in the industry right now, so Discover gets highlighted. LightStream’s maximum APR is 25.99% which is about as high as you should expect from a lender that caters to people Good or Excellent credit. Discover’s maximum is 24.99%. So Discover wins at the top rate as well.

I would say about half of all lenders don’t charge an origination fee. LightStream and Discover are among the half that do not charge origination fees.

LightStream will offer you a 0.5% discount if you sign up for autopay when you accept the loan. Discover does not have any discounts.

LightStream does not charge a late fee. Discover charges a $39 late fee, which is the highest I have seen from all the lenders that we track.

LightStream will accept a cosigner, but they call them co-applicants. Discover does not accept cosigners on their personal loans. A cosigner is someone who agrees to pay off your loan if you fail to repay it. If you can qualify for the loan that you need, there is little reason to entangle a loved one in the process. But, if you have a spouse or loved one that has a stronger credit profile than you do, add them as a cosigner might make all the difference in getting the loan you need. It’s good that LightStream offers this option.

If you are using the loan to consolidate credit card balances of other debt, LightStream will not directly pay off those other creditors with the proceeds of the for you. Discover, on the other hand, will. It’s convenient when a lender will do that, but it also shows that the lender knows that the loan will replace other debts and not stack on top of them. Because of that, the new loan won’t change your debt-to-income ratio. That should make it easier to be approved by them. Discover gets credit for giving customers this option.

While LightStream doesn’t restrict which debts you can consolidate, Discover will not use the proceeds to pay off Discover credit card balances. So, if you have Discover credit card balances that you would like to consolidate, you might need to find a different lender.

Let’s summarize what we’ve learned about personal loans offered by LightStream and Discover.

Both LightStream and Discover have their fare share of green. Lightstream has a few features that Discover does not have. Discover has slightly lower APRs, but LightStream’s APRs are in the same general pallpark. I think they are both pretty good lenders. But let’s be honest, the real issue is which company would give you the money that you need at the lowest rate. Each lender will have different criteria for deciding whether to approve you, how much to offer, and at what rate. That’s why we always recommend that before you accept a loan, you should shop around. Find the best deal. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about either of these lenders that we didn’t cover, leave a comment below. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!