LendingPoint $2,000 to $36,500 Personal Loan versus 60MonthLoans $2,500 to $10,000 Personal Loan. Detailed Review Across 11 Criteria.

We’re going to compare personal loans from LendingPoint and 60MonthLoans. We’ve spent years working in the lending industry and we track dozens of lenders. We want to break down these two lender so you can see which one might be better for your situation.

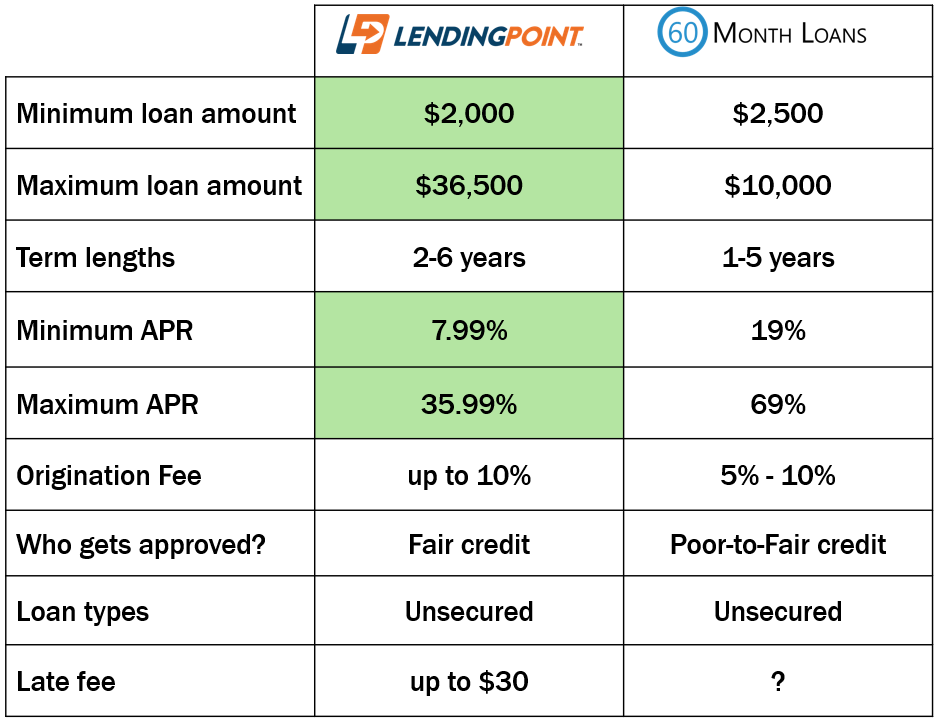

The first thing we are going to look at is the loan amounts that they offer. LendingPoint’s minimum loan amount is $2,000. 60MonthLoans’ minimum is $2,500. So, even though the difference isn’t all that significant, LendingPoint does have more flexibility on the low side, so I am going to highlight them.

If you are looking for a more substantial amount of money, LendingPoint will lend up to the curiously un-rounded number of $36,500 and 60MonthLoans tops out at $10,000. LendingPoint gets the credit for the higher loan amount. For both of these lenders, it’s important to remember that the amount that they offer you will depend on your particular financial situation.

LendingPoint personal loans have terms between 2 and 6 years. Contrary to their name, 60MonthLoans will lend for as short as 1 year and maxes out at their 60 months, or 5 years. Neither lender will charge a prepayment penalty, so it’s always a good idea to pay the loan off early. The way to save the most money on interest is to make as many extra principal payments in the first year of the loan.

Now let’s look the cost of the loans. LendingPoint’s minimum APR is 7.99% which is respectably low in this day and age. Happy Money’s minimum is 19%, which foreshadows who they lend to. We’ll get to that shortly. LendingPoint does get credit for having the lower APR. LendingPoint’s maximum APR is 35.99% and 60MonthLoans’ top rate is 69%. LendingPoint gets highlighted on the top APR as well.

LendingPoint will charge an origination fee that will depend on the state in which you live and could go up to 10%. 60MonthLoans is a little more clear about their origination fee range. It’s between 5% and 10%. I won’t highlight either of them because they feel pretty much the same. The origination fee is a percentage of the borrowed amount and comes out of the proceeds of the loan. So, if you borrow $10,000 and have a 5% origination fee, you will receive $9,500 but will still need to repay the $10,000. Remember that the origination fee is accounted for in the APR. The APR is the origination fee plus the interest rate. All things being equal, you want a lower origination fee if you plan on paying off your loan early. Paying off early will save you on the interest you would have paid, but you don’t get a reimbursement of the origination fee.

LendingPoint lends to people with fair credit and might lend into the bottom of the “good” range: people with credit scores between 620 and 700. 60MonthLoans probably dips into the poor range, but probably not too far: people with credit scores between 600 and 680. But, these are only guidelines. Lenders don’t usually use credit score to determine eligibility. They usually use information like payment history, debt-to-income ratios, utilization, income…stuff like that.

Both LendingPoint and 60MonthLoans lends only unsecured loans. This means that they do not require collateral—like the title to your motor vehicle—in order to apply. This also means that if you struggle to repay the loan, they can’t seize any of your assets as repayment. I generally think it’s a good idea for personal loans to be unsecured. However, securing a loan can make it easier to be approved, or to get a better rate than you otherwise would. Still, neither of these lenders offer secured loans.

LendingPoint says that if you are late on a payment, they will charge you “up to $30.” I am not entirely sure why it isn’t a set number. It could be that they are matching state regulations. But, you do need to know that $30 is a high fee in the industry. It’s not the highest, but it is awfully close to being the highest. 60MonthLoans is even more unclear. They do not report whether they charge a late fee or not.

So, let’s summarize what we’ve learned about personal loans offered by LendingPoint and 60MonthLoans.

LendingPoint clearly beats out 60MonthLoans in nearly every category. LendingPoint has a more flexible range of lending amounts, has better overall rates, and is a bit clearer about their policies. But I will say that because both of these companies lend to people with fair credit, you never know whether you are going to be approved or not. This is the space where slight changes to your payment history, stability of income, debt-to-income ratio, or any number of other metrics can be the deciding factor on whether you are approved or not. That’s why we always recommend that people with fair credit should apply to at least 3-4 lender before you make a decision. It’s very possible that one lender will approve you where another won’t. Each company has their own algorithm for making decisions. So, whatever you do, you should make sure to shop around.

At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about either one of these lenders that we didn’t cover, leave a comment below and we will try and answer it. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!