Summary

Personal loans are a very flexible form of credit. They can vary from $200 to $100,000 and can be used for a wide range of purposes. It is a good idea understand how personal loans work before taking one. Knowing how they can affect monthly budget, credit score, and overall financial wellbeing is important. Borrowers should understand the fees, interest rate, and structure of the personal loan before accepting it.

Key takeaways

- Personal loans typically range from $2,000 to $50,000.

- The easiest way to get approved is through with The Yukon Project loan market place.

- You can get a personal loan with bad credit.

- Interest rates on personal loans can be as low as 8%.

- You can get a personal loan in 24 hours or less. Higher loan amounts may take a few days or more.

- Read the loan terms carefully, look out for prepayment fees, late fees, and any other charge that is not a part of your regular loan payment.

What are personal loans?

A personal loan is a type of loan that an individual borrows from a financial institution, such as a bank, credit union, or a lending company for personal use. A personal loan can be secured or unsecured and is usually paid back over time in installments.

How personal loans work

Personal loans usually have a fixed interest rate, a set repayment period, and a fixed monthly payment. After accepting a loan, the lender will send the money to your bank account. Then each month you will make a payment to repay the loan.

Before you accept a loan offer, the lending company or bank must present you with the terms of the loan offer (this is a legal requirement). You can find this information in what is called a “TILA” box. “TILA” stands for Truth-in-Lending disclosure and it will include the annual percentage rate (APR) of the loan, any finance charges, the amount borrowed, and the amount of the regular payment.

What are personal loans used for?

The best thing about how personal loans work is that they can be used for a variety of purposes. This includes debt consolidation, home improvement, medical expenses, or even unexpected expenses. Some financial institutions may use the purpose of the loan as part of their decision to lend to you.

How much can I borrow for a personal loan?

Personal loans can be as small as a few hundred dollars and as much as $100,000. Most personal loans are between $2,000 and $50,000. Like most loans, the amount you can borrow is determined by your credit worthiness and income. The characteristics of the loan, like whether it is secured or unsecured will also impact how much you can borrow.

How long do I have to pay back a personal loan?

The length of the loan, also known as the term, is provided when the loan is offered. For small loans, the term can be as short as a few weeks. Most personal loans come with terms ranging from 2 to 5 years. However, loans less than $5,000 may have shorter repayment terms. Meanwhile, very large loans may be repaid over 10 years.

How hard is it to get a personal loan with good credit or bad credit?

The biggest factors in deciding whether you can get a personal loan includes the amount you need, your creditworthiness, and how large a monthly payment you can support on your current income. For small dollar personal loans, a company is unlikely to do rigorous underwriting. That means receiving a loan for under $1,000 may not be difficult. However, your creditworthiness will impact the terms of the loan, like the interest rate and the payback period.

These three components interact with each other. For example, if you have bad credit and you are approved, it may be for a lower amount even if your income is good. You may also be offered a higher interest rate.

The following table is a rough rule of thumb on what credit score is needed to obtain for the following loans. (Of course, this is a very rough idea. Underwriting standards are different for every company, so the only way to know for sure what you can qualify for is to apply.)

| Credit Score | Personal loan |

| Good credit | Whatever your income can support with the best APR available |

| Fair credit | Will qualify for some loans, but amount is limited and interest rate will be higher |

| Bad credit | Might only qualify for secured loans at a high rate |

| No credit score | Might only qualify for secured loans at a high interest rate |

What is a low interest rate APR for a personal loan in 2023?

When borrowing money, it is always better to get the lowest price you can get. A good APR for a personal loan is the lowest interest rate that your situation can get. That is why it is often important to shop around. Applying to more than one company is the most effective way to ensure that you are getting a good rate for the loan that you need.

- 12% is a good APR for a personal loan if you have good credit, but you may be able to do better if you have good or excellent credit. The APR may be higher if you borrow less than $5,000.

- 18% is a good APR for a personal loan if you have fair credit, but you should be able to do better if you have good credit and a reasonable income. The APR may be higher if you borrow less than $5,000.

- 25% is a good APR for a personal loan if you have poor credit. The APR may be higher if you borrow less than $5,000 and you may have difficulty being approved.

If you have poor credit, you might struggle to get an unsecured personal loan below 36%. If you have fair or poor credit and need a loan your best rate will be for a secured loan. But, you need to be aware that a secured loan comes with its own risks.

What is an unsecured personal loan?

An unsecured personal loan is a loan that does not require collateral. In other words, unsecured loans are not guaranteed by an asset. A lending company or bank will not be able to repossess borrowers’ cars, foreclose on their homes, or seize their bank accounts if they default.

What are the advantages of an unsecured personal loan?

The advantage to having an unsecured personal loan is that the company lending you money will not be able to take your assets. Many people who need to borrow money for an emergency do not have an asset that they could put up for collateral. Unsecured loans allow people to borrow when they don’t have title to a car or other asset that could act as collateral for the loan.

What are the cons of an unsecured personal loan?

Unsecured personal loans require more comprehensive underwriting because the lender must be more careful about whether someone would be able to pay them back. That means that it is harder to qualify for unsecured personal loans and the interest rate on the loans will be higher.

What is a secured personal loan?

A secured personal loan is a loan that requires collateral or an asset can be taken if the loan is not repaid.

What are the cons of a secured personal loan?

Perhaps the biggest con of secured personal loans is that if something happens and borrowers are unable to pay the loan, the lending company can seize the collateral in order to cover the principle. This means that someone who defaults on a secured personal loan could end up worse off than they were before taking the loan.

What are the advantages of a secured personal loan?

Although secured personal loans carry the risk of losing the asset if you default, they do have some advantages. Lenders often approve people who have an asset that can secure a loan more often and for higher line amounts because they are exposed to lower risk if the borrower defaults on the loan.

Is it easy to get approved for a personal loan?

There are many companies lending money in the United States right now and so the chances of being approved for a personal loan has never been higher. However, every lender has their own process for deciding who to lend money to. Some lenders want to only lend money to people with excellent credit. Others are willing to lend money to borrowers with fair or even poor credit. If approved for a personal loan, borrowers with poor credit will usually qualify for a higher interest rate and a lower line amount.

Can anyone get a personal loan?

There are a broad range of companies who are willing to lend money. Some lenders even specialize in lending money to people with damaged credit. However, not everyone can qualify for a personal loan. Some people do not have enough credit history which means that companies may not have any way of knowing whether lending them money would be too risky. Other people have had problems with their credit recently and may not be able to find a company to take a chance on them.

There are personal loans for people with bad credit, but the lenders will charge a higher interest rate to cover the risk of default.

Personal loans for people with good credit are available with non-bank lenders as well as through banks and credit unions.

What is an example of a personal loan?

The following are a couple of examples of what a personal loan might be:

What would the monthly payment for a $3,000 loan be?

A $3,000 loan with a term of 2 years and at an interest rate of 19% would cost approximately $166.20 per month. Below is what the TILA box might look like for this loan. However, there are a number of things that could be different about a $3,000 loan that could make the loan slightly different (a few dollars) even if the term and APR are the same. Changing the term or the APR could make a very large difference.

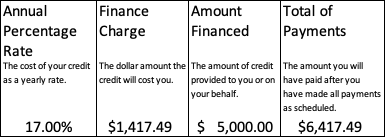

How much would a personal loan for $5,000 cost per month?

A $5,000 loan with a term of 3 years and at an interest rate of 17% would cost approximately $178.26 per month. Below is what the TILA box might look like for this $5,000 loan. All loans will vary a little, but this is a reasonable expectation of what you would get.

How much would the payment be for a $20,000 personal loan for 5 years?

A $20,000 loan with a term of 5 years and at an interest rate of 12% would cost approximately $444.89 per month. Below is what the TILA box might look like for this $20,000 loan. With great credit you may be able to get a better interest rate than 12% which could lower your payment substantially.

How do you calculate the monthly payment on personal loans?

Calculating the monthly payment on personal loans is harder than it sounds like it should be. You might think that all you have to do is divide up the principle into the number of payments and then add interest to the payment. But, it’s a lot more complicated than that. Since personal loans charge an interest rate, the interest you would pay is based on the total money you still owe, not on the original amount.

Monthly payments are balanced so that payment is the same from the beginning to the end of the loan. That means that a personal loan’s first payment is mostly interest expense. Conversely, the last payment is mostly principle. Instead of attempting to do the math, the easiest thing to do is find a payment calculator online.

Is a personal loan a good idea?

It is always important to be careful when considering taking on more debt. You want to make sure taking a personal loan a good idea in your situation.

Personal loans can be an great way to solve financial emergencies, improve your life, or give you a chance to take advantage of an opportunity. Some of the following situations might be good reasons to take out a personal loan:

- Repair your car so you can get to work

- Have an important medical procedure done

- Starting a personal business

- Buy something important that you can pay for over time

How personal loans work, interest and fees?

Most personal loans are installment loans which means that they are paid over time with monthly or twice-monthly payments. Lending companies charge interest on the outstanding balance. The interest is stated as a yearly rate, but it is calculated daily. So, if the interest rate was 36.5%, the daily interest charged on the existing principle would be 0.1% per day (36.5% ÷ 365 days). If the principal balance is $1,000, the interest incurred for the day would be $1 (0.1% × $1,000). Payments are calculated so that the payment is the same throughout the life of the loan. This means monthly interest payment goes down as the principal is paid down. Lenders do this so it is easier for borrowers to plan their loan payments.

Is it a good idea to pay off personal loans early?

Lenders charge interest for personal loans on a daily basis. Therefore, making extra payments to principal will always save money on interest. Making extra payments early in a loan will save the interest expense on that payment throughout the life of the loan.

Paying off a personal loan early may not be a good decision if it includes a prepayment penalty. If the loan has a prepayment penalty, it is important to calculate the difference between the interest dabbed and the fee charged.

Sometimes paying off a personal loan early is the best decision just to decrease your overall debt.

Do personal loans report to the credit bureaus?

Most companies and banks that offer personal loans report payments to the credit bureaus (Experian, Equifax, and TransUnion). You should see the details on your credit report if the lender reports to that credit bureau. Note: you may not see it show up on your credit report for two or three months after taking out the loan because there is a meaningful lag in the reporting process.

Do personal loans help my credit score?

Making consistent, on-time payments is incredibly important to building a strong credit score. However, late payments and defaults reported to the credit bureaus will make a meaningful decrease in a credit score. Personal loans can be very good for your credit score if you are always on-time with your payments. They can be bad for your score if late payments are reported, even if you are only rarely late.

Will paying off my personal loan improve my credit score?

Credit scores are very complicated so it is not always clear whether paying off a personal loan will improve your credit score. The impact to your credit score will depend on how long you had the loan, how much you owed, and what other credit is on your credit report. That means it’s possible to decrease your credit score some by paying off a personal loan. This can be frustrating.

Keep this in mind. Decreasing your debt levels is the responsible and financially sound choice. Instead of focusing on the credit score, consider the following. Paying off a personal loan will decrease your debt and free up money in your monthly budget. You can use that money to pay down revolving debt (like credit cards) which is good for your credit score. Or you can build a savings account with it!

What is the easiest way to be approved for a personal loan?

The easiest way to be approved for a personal loan is to apply through a marketplace website that will find several lenders who will pre-approve you. Check out our marketplace if you want to see which lenders will pre-approve you.

What does it mean to be pre-approved for a personal loan?

Being pre-approved for a personal loan usually comes after you give a lender permission to do a soft pull of your credit report. The lender looks at the initial information you share with them to determine you are likely to qualify for a loan. A lender, at that point, may even make a detailed offer. If you take the offer, the lender will then do a hard credit pull and make the final determination on your approval.

What does it mean to be pre-qualified for a personal loan?

A lender may pre-qualify a borrower for a loan based on the fact that the borrower appears to meet the lender’s criteria. This does not guarantee approval. The borrower must still submit an application and go through the underwriting process. If the borrower’s situation still meets the lender’s criteria, the lender will give the lender an approval.

What is the difference between being pre-approved and being pre-qualified?

Some lenders use pre-qualified and pre-approved interchangeably because these terms are very similar. Both pre-approved and pre-qualified mean that based on initial information, the potential borrower meets the lender’s loan criteria. There are additional checks that must still be completed to get a loan which cannot be done before the pre-approval.

Pre-approval does have a slightly different legal meaning in some states. It’s a difference in the additional review a lender is allowed before providing a loan.

If I was pre-qualified for a personal loan, why was I denied when I applied?

Many people get a letter in the mail stating that they have been pre-qualified for a loan. Sometimes they apply but are still rejected. The reason for this is often because your financial situation changed from the time the lender pre-qualified you to the time that you applied. As many as 25% of people with fair or poor credit are denied even when they are pre-qualified.

What should you do before you apply for a personal loan?

This is a highly personal decision, but you should ask yourself the following questions before applying for a personal loan:

- Can I afford the payment?

- How important is it that I borrow this money?

- Would my situation be worse if I wasn’t able to take out a personal loan?

- Do I have a plan for how I will pay off this personal loan?

- Do I have access to a better way to solve my financial emergency?

How long does it take to get a personal loan? How quickly can I get a personal loan?

You can get a quick personal loan, even instantly. The higher the line amount you’re seeking, the more likely the underwriting process will take a little bit of time. You can get a small dollar personal loans, those under $3,000, in a matter of hours although they usually take a couple of days. Larger loans may take anywhere from two days to a couple of weeks.

The application itself is also becoming easier and easier. With the advent of digital banking and credit bureaus, most people have everything they need for an application at their fingertips.

What do I need to apply for a personal loan?

While underwriting processes differ lender by lender, most will require the following items when you are applying for personal loans:

- Access to your credit report

- Proof of income

- Proof of identity

- Access to your bank account

Most lenders today will deposit loan proceeds directly into your checking account and withdraw payments through ACH (automatic clearing house). More and more lenders are also looking at bank account data in the underwriting process.

Why does the lender want to log into my bank account when I apply for a personal loan?

For a generation, underwriting has centered on data found in a person’s credit report. The problem is that data in a credit report is weeks, sometimes months old. Credit reports do not include income. They also don’t show loans that do not report such as payday loans and buy-now-pay-later. Lenders are learning that looking at bank information gives more information when deciding whether to lend money.

Will applying for a personal loan hit my credit report?

The answer to that question is more complicated than you might think. If you seek pre-approval from lenders or using a loan matching tool like The Yukon Project’s loan program, the companies use a “soft” credit pull to see if you’re eligible for a loan. Soft credit pulls do not affect your credit score. If the lender does a hard credit pull when you apply it will show up on your credit report. A hard inquiry is required to take out a loan. A hard credit inquiry could negatively affect your credit score by up to ten points, possibly a little more. It usually bounces back in two to three months.

If a lender does a soft credit inquiry and approves you for a loan, you will receive a hard inquiry on your credit report if you accept the loan.

Will applying for several personal loans at once hurt my credit score?

Most major credit score algorithms recognize when a person applies to several companies for a personal loan in a short window of time and do not penalize them. They see that as a responsible behavior in shopping around for the best option. Accepting several loans or the applying with lenders over several weeks or months will likely lower your credit score.

Will taking a personal loan hurt my credit score?

Taking a personal loan can affect your credit score in a couple of ways. By increasing your debt load, it could lower your credit score. Making regular, on-time payments will be a positive factor in your credit score, though, because consistent on-time payments are such an important part of a credit score.

Where can I find the best personal loans online?

One of the best ways to find personal loans online is to visit our marketplace page where you can shop dozens of lenders online. Our process will also ensure that the personal loans are offered in your area.

What is the difference between personal loans and installment loans?

Installments loans is a broad category that include most personal loans. Installment loans are repaid over time in installments.

What is the difference between personal loans and payday loans?

Personal loans is a broad category that includes both low-dollar loans and larger loans that take years to pay off. Payday loans are small loans that need to be paid off in full on the borrower’s next pay date. For more information, check out our section on payday loans.

What is the difference between personal loans and lines of credit?

Personal loans provide a lump sum with a fixed payoff schedule while a line of credit provides access to funds that can be used as needed. Personal loans typically have a fixed interest rate. Lines of credit often have a variable interest rate that changes depending on macroeconomic conditions.

What should I watch out for when I take a personal loan?

When you are applying for personal loans, you can often be stressed as you look for money. In that moment, you might be happy that you are approved and don’t look closely at the terms of the loan. Taking an extra moment to ensure you understand what you are getting into can prevent added stress in the future.

Here are a few things you should look for when considering a personal loan out from a company.

- Unexpected fees: You should always check the loan agreement to see what other fees the lener may charge.

- Reviews: Don’t just look at a lender’s star rating. Read some of the comments to see whether the company will be a good partner in your financial journey.

- Monthly payment: It is important to determine whether you can comfortably fit the payments into your budget. Pay particular attention to the payment schedule. You don’t want to find out too late that the payments are made twice a month and not monthly.

- The term: How long is it going to take you to pay the loan off? A longer term will lower your monthly payment, but it will extend how long you’ll be in debt. It could also mean paying a lot more in interest over time.

Finally, before you decide to take that personal loan, you should make a plan for how you are going to pay the loan off. Look forward a couple of months and determine if there are ways you can make extra payments or how you will make sure the payments fit into your monthly budget. Having a plan before you accept the loan can help you get ahead of things early on.

What are some of the fees that might come with personal loans?

Before you accept a personal loan, you should to check to see if the lender has any of the following fees: interest, origination fee, late fee, application fee, processing fee, underwriting fee, prepayment penalties, and credit insurance. If you only compare the interest from one company to another, you might miss that one of the lenders includes an origination fee and a prepayment penalty which could make the loan less attractive even if it has a lower interest rate.

These are the fees you should watch out for when you think about accepting a lender’s personal loan offer:

Interest

Interest is the cost of the loan as a percentage of the outstanding balance. It’s charged as a percent of the balance for each day the loan is owed. While many people call this the APR (annual percentage rate), that is incorrect. The APR will also include unavoidable fees like application fees, origination fees, etc. The APR will tell you the overall cost of the loan. The interest rate will help you understand how much you can save when paying the loan off early.

Origination fee

Some lenders will charge an initial fee when originating the loan. The origination fee is usually calculated as a percentage of the borrowed amount. Origination fees increase the overall cost of the loan. Unlike the interest rate, cannot control this cost by paying the loan off early.

Application, processing, underwriting fees

Some lenders will charge a fee that will help them cover the cost of underwriting and processing the application. They might call it an application fee, a processing fee, or an underwriting fee. This amount is usually a fixed cost regardless of the size of the loan.

Late fee

Late fees can be an important way that a lender makes a profit. Some lenders charge borrowers if they do not make their payment on-time. Typical late fees are usually between $10-15 but some lenders may charge much more.

Prepayment penalty

A prepayment penalty is a fee that a lender charges if the loan is paid off before the term is completed. Prepayment penalties can discourage borrowers from getting out of debt.

Credit insurance

While technically not a fee, credit insurance can add to the cost of a loan. Warning: credit insurance is not usually included in the loan APR. If a lender requires credit insurance, you should consider it in the overall cost of borrowing. Credit insurance usually ensures that the loan is paid off if something happens such as job loss, becoming disabled, or even death.

What are the risks to taking out a personal loan?

The risks to taking out a personal loan is that the payment will become a burden on your monthly budget. Every debt payment in your budget reduces your financial flexibility. This means you have less money available to you when financial emergencies that come up.