Personal Loan Detailed Comparison Across 10 Criteria between Axos $50,000 Personal Loan and Truist $100,000 Personal Loan

We’re going to compare personal loans from Axos and Truist. We’ve spent years working in the lending industry and we track dozens of lenders. We want to break down these two lender so you can see which one might be better for your situation.

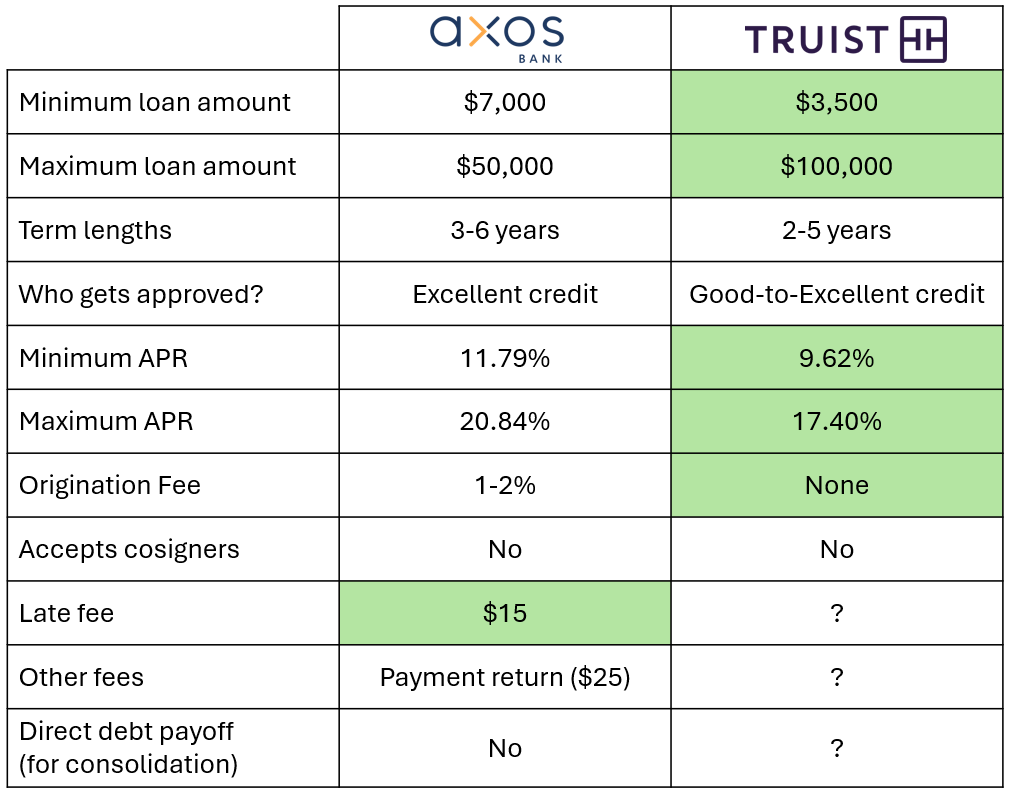

The first thing we are going to look at is the loan amounts that they offer.

Axos doesn’t offer a personal loan less than $7,000, so they aren’t going to be the option for filling a short-term emergency. Truist doesn’t lend less than $3,500 for a personal loan. That’s still higher than a lot of lenders, so if you are looking for just a little bit of money, neither of these banks is probably your best best. But, Truist has the lower amount, so we’ll highlight them. If you are looking for a more substantial amount of money, Axos lends up to $50,000 and Truist lends up to $100,000. Again, Truist wins for the top amount.

Axos doesn’t lend for terms shorter than three years, but they don’t have a prepayment penalty, so you can always pay off the loan early. Truist will lend between 2 and 5 years.

Common to a lot of banks, Axos and Truist cater to people with Excellent credit or—in Truist’s case—at least Good credit. I am guessing that you would struggle to get approved by either of these banks if your credit score was not higher than 660. But they probably don’t make a decision based on credit score, so the only way to know whether you would be approved with your specific credit profile is to apply.

Now let’s look at the cost of AXOS and Truist Personal Loans.

The minimum APR for Axos is 11.79% and for Truist it’s 9.62%. Getting an APR below 10% is not easy in this day and age, so Truist gets highlighted. Axos’ top APR is 20.84% while Truist tops out at 17.40%. So, Truist wins the top number as well. 17% is actually quite a low top number. That’s one of the things that makes me think that Truist is going to be rather stringent with who they accept.

Axos charges an origination fee of between 1% and 2%. That’s a really low origination fee. Low enough, actually, that I wonder why they would bother to have one at all. Truist, on the other hand, doesn’t charge an origination fee at all. So, they win that category as well. The origination fee is accounted for in the APR. The APR is the origination fee plus the interest rate.

Neither one of these lenders will allow you to include a cosigner or coapplicant to your loan. A cosigner can boost your chances of being approved, especially if they have a strong credit profile.

Axos will charge a $15 fee if you are late with one of your payments. If they attempt to draw your payment using ACH authorization and the payment fails, they will also charge you a fee. This is where Truist is not terribly forthcoming. It is not at all clear if they charge a late fee or any other fees. That’s a little disconcerting. I am going to give the late fee category to Axos because $15 isn’t egregious. But I am not going to assign the other fees because $25 failed payment fee is actually quite high.

If you are using the loan to consolidate credit card balances or other debt, Axos will not use the loan’s proceeds to pay off your other debt for you. It is not clear whether Truist will do it or not. I like it when companies will do that because they understand that the loan is meant to replace your other debts and not just stack on top of them. The fact that neither of these companies will do it probably means that it would be harder to get approved with them if you want a loan for the purpose of consolidating debt.

Let’s summarize what we’ve learned about personal loans offered by Axos and Truist.

Truist wins most categories, but I struggle to give them a full-throated recommendation because they just aren’t very clear about their policies. That is actually rather rare for a bank. They are usually the most clear about things. So, that’s a bit of a yellow flag, in my mind. Even though we aren’t seeing much green on the Axos side, I don’t think they look bad. As is often the case, the most important issue is whether you can get the money you need at the lowest possible price. If Axos can do that, there’s no reason not to use them. But before you accept a loan, you should always shop around. Lenders each have their own algorithms for deciding who to approve. You could be rejected by one and still be accepted by another.

At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about either of these lenders that we didn’t cover, leave a comment below. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!