Personal Loan Detailed Comparison Across 10 Criteria Between an Avant Personal Loan and OneMain Financial Personal Loan!

We’re going to compare personal loans from Avant and OneMain Financial. We’ve spent years working in the lending industry and we track dozens of lenders. We want to break down these two lender so you can see which one might be better for your situation.

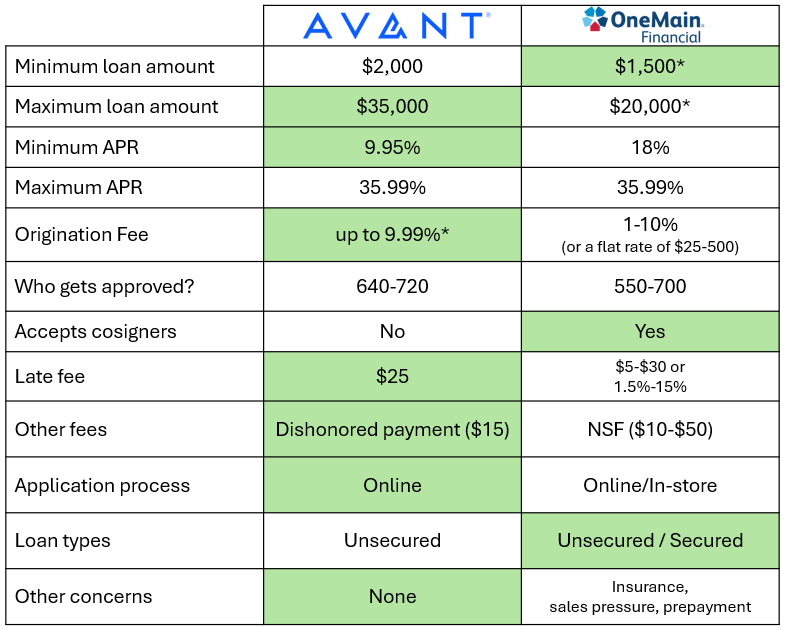

The first thing we are going to look at is the loan amounts that they offer.

Avant’s minimum loan amount is $2,000 and OneMain will issue loans as low as $1,500. So, if you are looking for a little bit of money to handle an emergency, OneMain offers a little more flexibility on the low side. If you are looking for a more substantial amount of money, Avant will lend as much as $35,000 while OneMain tops out at $20,000. I put an asterisk next to OneMain’s minimums and maximums because in some states these numbers change. For instance, in 6 states the minimum is at least $2,000. And in four states the maximum is below $14,000. Avant definitely has more flexibility on the high side.

For both of these lenders, it’s important to remember that the amount that they offer you will depend on your particular financial situation.

Loans from Avant have terms between 1 and 5 years. OneMain’s terms range from 2 to 5 years. If you are borrowing only $1,500 from OneMain, do not take two years to pay it back.

Avant’s minimum APR is 9.95% which is a very respectable bottom rate in this day and age. OneMain’s minimum is 18%. Both of them have maximum APRs that cap out at 35.99%.

Avant charges an origination fee up to 9.99%, but you will notice that I put an asterisk in there. That’s because Avant actually calls it an administration fee which has a unique property. If you pay off your loan early, Avant will reimburse you a prorated amount of the administration fee—at least as long as the fee was more than 5%. Avant is the only lender I know that does this.

OneMain’s origination fee ranges from 1% to 10%. But in some cases it would be a flat rate of $25 to $500. Why the confusion? Well, OneMain will charge the most that they can given the state laws in which they operate. That means that it will depend on what your state’s regulations limit. I am going to highlight Avant for its origination fee.

Keep in mind that the origination fee is a percentage of the borrowed amount and comes out of the proceeds of the loan. So, if you borrow $10,000 and have a 5% origination fee, you will receive $9,500 but will still need to repay the $10,000. Remember that the origination fee is accounted for in the APR. The APR is the origination fee plus the interest rate. All things being equal, you want a lower origination fee if you plan on paying off your loan early. Avant is the only lender I know that will give you a reimbursement of your origination fee you pay the loan off early.

Avant targets customers with Fair-to-Good credit—credit scores between 640 and 720. OneMain is willing to lend to people below 620. Just over half of their borrowers have credit scores below 620. The lower you go down in their ranges, the less likely you are to be approved. These are guidelines. Lenders don’t usually use credit score to determine eligibility. They usually use other information in your credit file: payment history, debt-to-income ratios, utilization, stuff like that.

Avant does not accept cosigners on their loans, but OneMain will. A cosigner is someone who agrees to pay off your loan if you fail to repay it. If you can qualify for the loan that you need, there is little reason to entangle a loved one in the process. But, if you have a spouse or loved one that has a stronger credit profile than you do, add them as a cosigner might make all the difference in getting the loan you need. It’s good that OneMain offers this option.

Avant charges a $25 late fee, which is a rather hefty fee. Not the highest in the industry, but certainly higher than most. OneMain charges $5 to $30 or it could be 1.5% to 15% of the late amount. Again, I believe state regulations will dictate what they can charge. But 15% of the late amount is an eye-popping number. So, you will want to keep an eye on what they will charge you in your state. I am going to give this category to Avant because of the simplicity.

Both companies will charge other fees as well. Avant charges a $15 dishonored payment fee if they attempt to take a payment and the check bounces or there’s not enough money in the account when they attempt to make an ACH draw. OneMain calls it an NSF (or “Non-sufficient Funds” fee). They will charge between $10 and a whopping $50. Fifty dollars seems so outrageously high that I have to double check my research every time I see it. And, yup, it really is $50.

With Avant, you can complete the entire application process and funding online. For OneMain Financial, you can apply online, but you will need to go into a store to complete the process. In store, you will verify your identity and sign documents. Going into a store doesn’t sound convenient, but it does allow you to get the money immediately. With Avant, you would have to wait one business day to get the money deposited into your account.

Avant lends in 46 states and OneMain in 44 states. This is meaningful because of OneMain’s requirement that you visit a OneMain Financial storefront to complete the process.

Avant only offers unsecured loans. OneMain offers both unsecured loans as well as loans that are secured with the title of your motor vehicle. OneMain might even push you to secure the loan in order to increase your chances of being approved. That’s a two-edged sword. Securing a loan can often help you get approved when you otherwise wouldn’t, but it also puts your collateral at risk. If financial trouble arises, you might find yourself in worse shape than you were before, especially if you lose your automobile in the process.

There are a few concerns that I need to bring up when it comes to OneMain Financial. OneMain has several different kinds of insurance that they will try and get you to buy. The cost of the insurance will not be accounted for in the APR, so paying for the insurance could make borrowing from OneMain Financial more expensive than you expected. Because you have to go into the store to complete the process, you might be subjected to some sales pressure. The last concern I have about OneMain is that they don’t make it easy to pay off the loan early. In fact, any extra payments you make will just pre-pay future payments rather than paying down the principal. That means you won’t actually save interest by paying early.

So let’s summarize what we’ve learned about OneMain Financial Personal Loans and Avant Personal Loans.

You can see that Avant wins more categories than OneMain Financial does. But, for many people, the most important two things are whether they can get the money they need at the lowest possible price. If your credit profile is a little weaker than you’d like it to be, OneMain might be the one that offers you money where Avant wouldn’t. You will need to balance the relief of getting the money you need with the potential risks of a OneMain loan, especially the difficulty in paying it off early.

Whatever you do, we always recommend that before you accept a loan, you should shop around. Make sure that you are getting the best deal your situation can get. At The Yukon Project, we’ve tried to make shopping around easy. If you visit our marketplace page, you can apply to any one of our other featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of the approved offers so you can pick the loan that’s best for you.

If you have any questions about either one of these lenders that we didn’t cover, leave a comment below and we will try and answer it. If you found this video useful, please like it and subscribe to our channel. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!