How To Pay Off Credit Card Debt FAST! We show you the math & savings. Take years off and save $$$.

The big take-away I want you to get from this video is you can pay off your credit card debt quickly, even if you have a substantial amount. There are a lot of options that you can pick from to find a solution that fits with your lifestyle. These options have a major impact on how long it will take and how much interest you will end up paying. I will show you how you can reduce your credit card payback time from 10 years all the way down to 2 years.

In order to do that, I am going to compare these 8 payoff strategies.

- Making the minimum payment

- Making extra principal payments every month

- Snowball debt payoff strategy

- Avalanche debt payoff strategy

- Velocity banking

- Balance transfer

- Debt consolidation

- Acceleration

I am going to walk you through the actual numbers, so you can see how each one works. I’ll show you how long it would take to become debt-free, how much interest you end up paying, and where things can go wrong.

We’ve spent years in the lending industry. We have analyzed the personal financial lives of tens of thousands of people. We want to use that experience to help you find the most efficient way for you to pay off your credit card debt.

We have based our analysis on $8,000 in debt across four different cards…which just happens to be the national average.

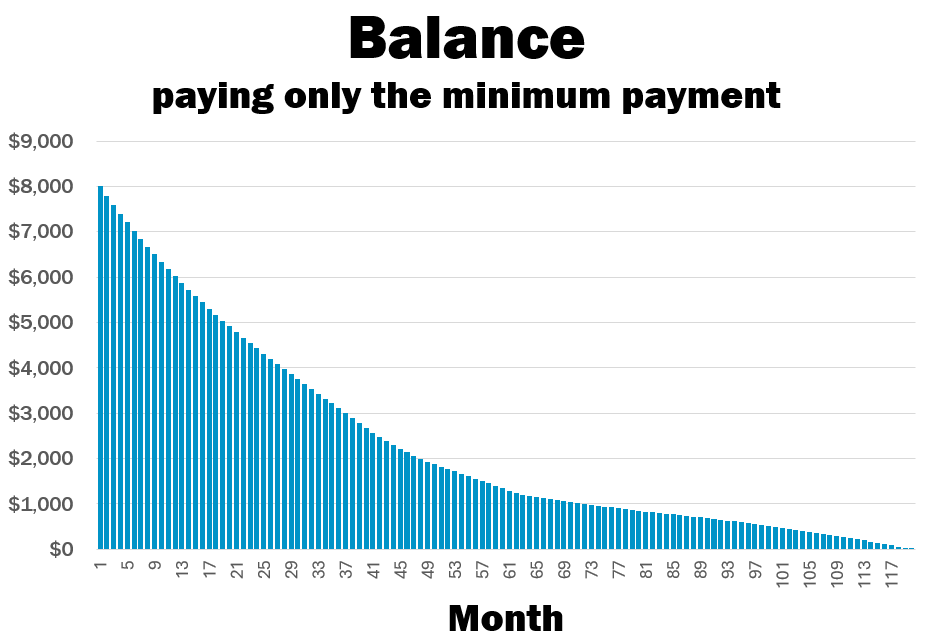

Making the Minimum Payment

Let’s start with “making the minimum payment.” This is the default option, after all. You just make the credit card’s minimum required payment every month. It should come as no surprise that this will keep you in debt a long time.

As you can see, it would take you just shy of ten years to pay off the balances. Over that time, you end up paying $5,206 in interest on top of paying the $8,000 back.

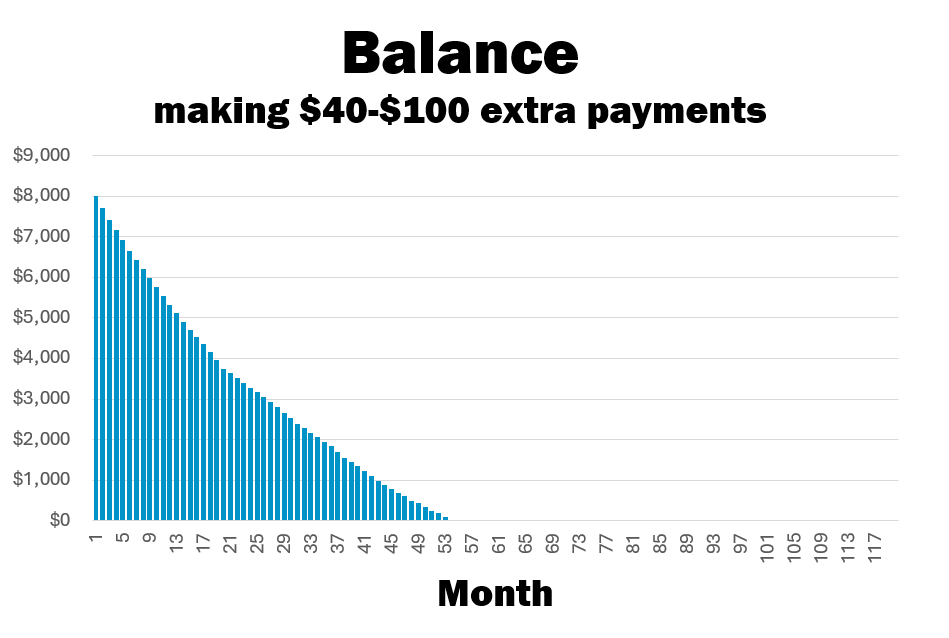

Making Extra Principal Payments

The key to getting out of credit card debt is paying more than the required minimum payment every single month. That may sound obvious, but it’s not always obvious how powerful that consistency can be. If you make an extra payment every month that is between $40 and $100, it can make a huge difference.

Instead of paying the debt off in 10 years, you are paying it off in 4.3 years. Over that time, you would pay $3,366 in interest. That saves $1,840 over only making the minimum payments every month.

Take note that the payments don’t need to be hundreds of dollars. Too often, people look at their total debt and get overwhelmed. They can’t imagine how they will ever come up with that amount of money. The key is just coming up with a little bit of money every month. Ideally, as your minimum required payment drops, you would be able to increase the extra principal you include. That’s what this next method demands.

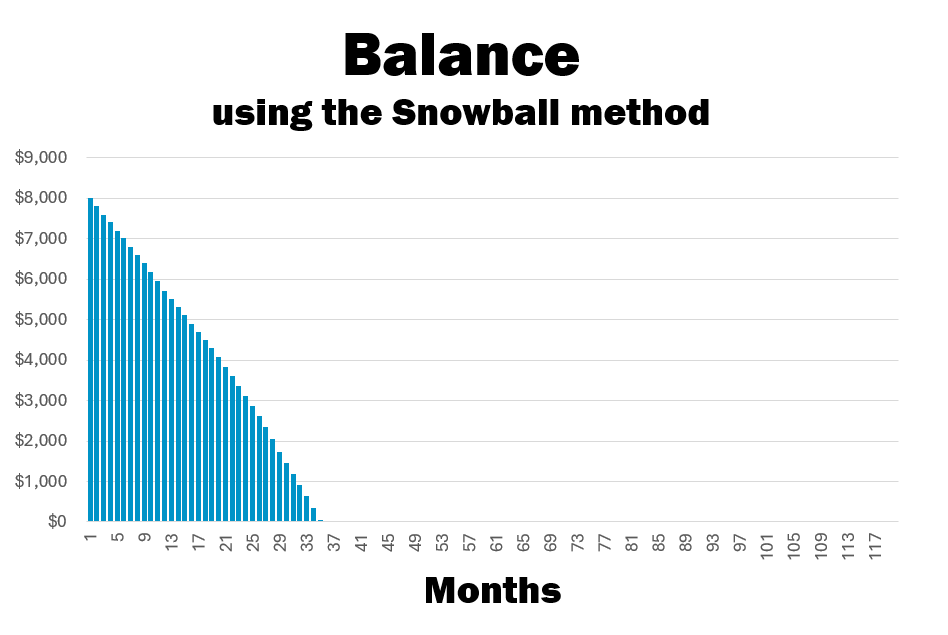

Snowball Method

Now let’s see what happens if you use the snowball strategy of debt payoff. The snowball strategy is based on the idea that a snowball rolling down a hill gets bigger and bigger. That’s what you are trying to do with your payments. In this strategy, you still pay the minimum payment on all of your debts, but you put all the extra money towards the smallest debt.

In our example, the plan is to pay off this $900 balance as fast as possible. When that’s paid off, you move the money you were paying to that debt and you put it and all extra payments against the next smallest debt. As you pay off the debts, your monthly payment gets bigger and bigger, like a snowball rolling down a mountain.

Let’s compare the snowball strategy with just making extra payments. Here is the balance by month of the snowball method. The yellow line is the balance for making extra payments. You can see that you get out of debt much faster. But, to be clear, the reason is because you are making more of an effort to maintain your payment size. Instead of just finding $40 to $100 over the minimum, you are trying to keep your payment up and rolling it from one debt to the next.

The key to being successful with the snowball strategy is to maintain a high monthly payment. That’s really why so many people recommend the snowball strategy. It’s all about psychology. It’s hard to do something consistently month after month after month. But, seeing tangible progress can keep us motivated. When you are getting rid of creditors, you feel like you are making progress. That’s why you get rid of your smallest debts first, because you can knock them off quickly. By the time you get to your bigger debts, your payments are bigger and you are making faster progress.

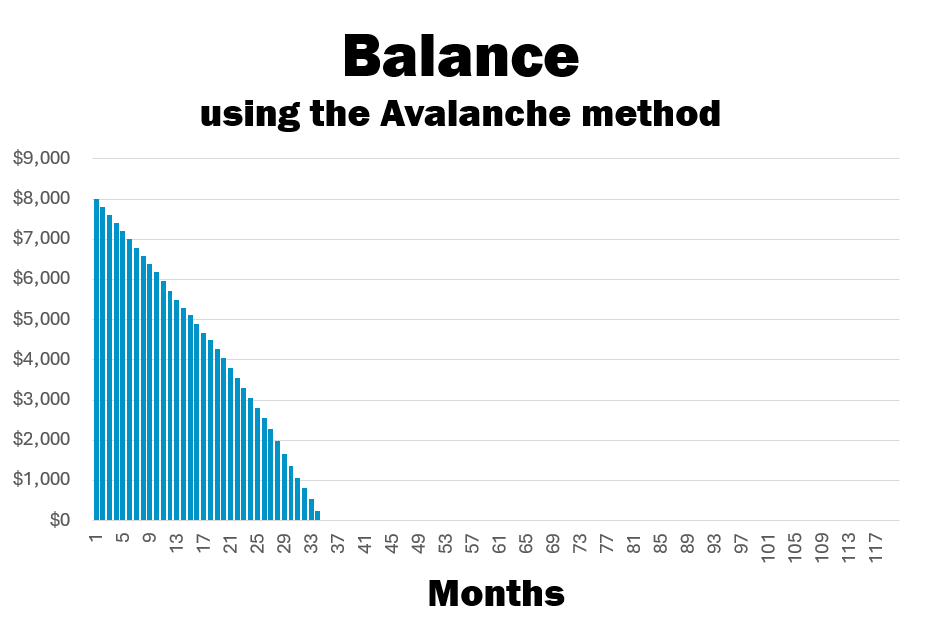

Avalanche Method

A less famous strategy is called the avalanche method. Like the snowball, it’s all about intentionally using your extra payments. Instead of putting your extra payments against the smallest debts, the avalanche method tells you to put them against the debt with the highest interest rate.

The rationale is pretty simple: interest is calculated at the daily level. So, if you can pay down the debt that charges the most interest, you pay less interest. More of your payment will go towards principal. Paying down principal saves on more interest. It becomes a virtuous cycle. Like an avalanche, you shake more interest loose which helps you make bigger payments which shakes loose more interest. In that way, your payments build over time.

How does the avalanche compare to the snowball method? With the avalanche method, you pay off the debt about a month quicker and you end up paying a total of $2,911 on interest.

That doesn’t seem terribly significant. But that is because, in this example, the card with the highest balance has one of the lowest APRs. If that card had one of the higher APRs, the difference would have been much more significant. And if you had a high interest loan, the avalanche method could save you a lot of money and time in the long run. The bigger the difference between your highest and lowest APR, the more money you will save with the avalanche method.

The power of the avalanche method can also be its chief problem, though. When your most expensive debt is one of your highest balances, it can take months or years to pay off. That could be demoralizing if it doesn’t *feel* like you are making progress, even if you *are* making faster overall progress.

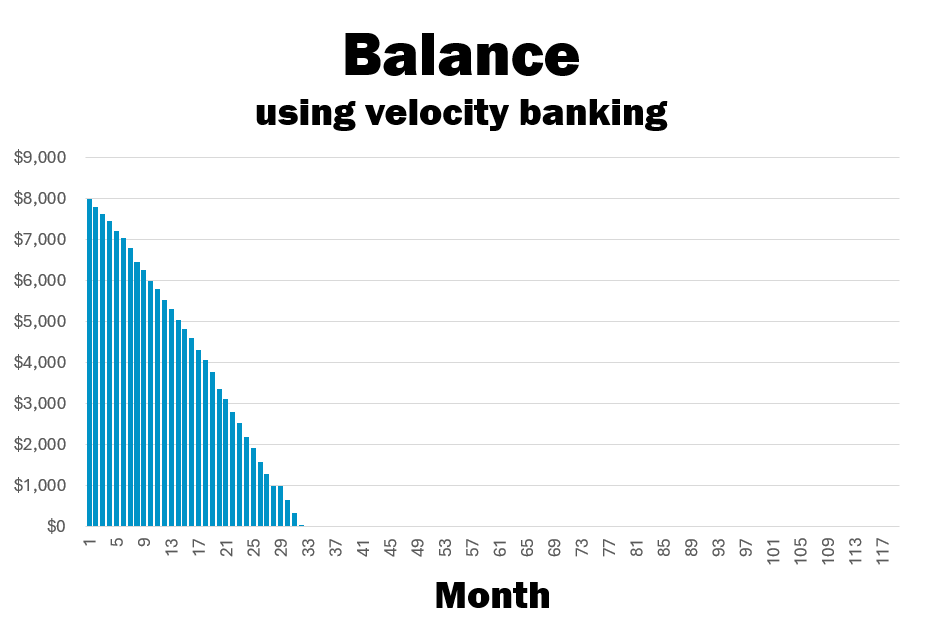

Velocity Banking

Now I want to show you the results of something called velocity banking. It has gotten a lot of interest lately. One of the biggest challenges of velocity banking is that it can be confusing. That confusion has caused a lot of people to do the math wrong when they analyze it. This leads some people to overstate its effects, like it’s some kind of magic bullet. But, I’m getting ahead of myself. The question is, what is it?

Velocity banking is based on the insight that interest is accrued at the daily level. Dropping your average daily balance will save you money on interest. Here’s how you do that: you put every free dime from your paychecks into paying down your credit card debt. Because you don’t have any cash left on hand, you make all your purchases for the rest of the month with your credit card. By the end of the month, you’ve built up your credit card balance again, but for most of the month, you have saved some money because your average balance was lower than it would have been if you just made end-of-the-month payments.

Let’s look at how long it takes to get out of debt using velocity banking. As you can see, velocity banking can be really effective. You can get out of debt in 39 months having paid only $2,327 in interest over that time. That compares favorably to the other methods we’ve looked at so far.

There are some risks to using velocity banking that you need to be aware of. First, because you are actively using your credit cards, you might spend more than you should. You might not even be aware of it. Ironically, that might mean that you are making smaller monthly principal-only payments than you would have using another method.

The second risk of velocity banking is that there comes a point when the interest you are paying on your monthly purchases is actually more than the savings you gain from using velocity banking. You can get caught in a period where you don’t really make progress. This is because credit cards immediately charge interest on purchases if you carry a balance from one month to another. You only get a grace period if you had paid off your balance the prior month.

The third risk of velocity banking is recognizing that not everything can be paid for with a credit card. You have to plan for those costs otherwise you get yourself caught without the money you need to meet your obligations. Mortgage or rent payments are easy to plan for, but bi-yearly insurance premiums, an unexpectedly high utility bill, or income taxes could trip you up. Cash advance fees or late fees could be more expensive than the interest you save in a month using velocity banking.

Finally, I do need to say that velocity banking only works for paying off revolving credit, like credit cards or lines of credit. You obviously can’t use this method to pay off an installment loan.

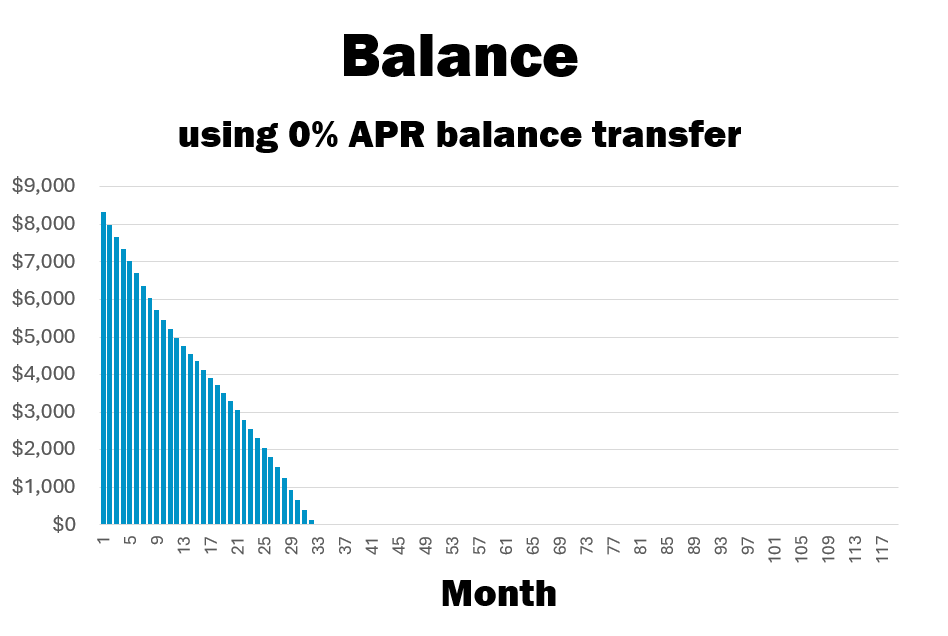

Balance Transfer

Credit cards can sometimes offer an introductory 0% APR period when you transfer balances from other credit cards. Obviously, they want your business. For many, this feels like a trap. Credit cards would not offer this service if they didn’t get something out of it, right? If you are struggling with credit card debt, isn’t adding another credit card the worst thing you could do? Well, the risks are obvious, but let’s look at what you could get out of it.

First off, the key to balance transfer is that the 0% APR introductory period. That can save you a lot of money in interest. The only question is what you do with that savings. Let’s assume that you get a card with 8 months of 0% interest. In our analysis, we include a 4% balance transfer fee. During the 8 months with no interest, it’s important that you are still making your payments, including any extra principal payments. Using that time to pay down the debt can be hugely beneficial. Get the balance as low as you can get it before the interest starts kicking in again.

In our analysis, you can pay off your debt in two years and eight months. That looks pretty similar to some of the other aggressive strategies. But the really cool thing is that you only spend $1,341 on interest during that time. That’s huge savings.

This can be a very powerful tool for getting out of debt, but you must avoid two temptations: first, you can’t use the interest-free period as a payment holiday. And second, you can’t run up your credit card balances again. If you think you might do one or both of those things, you should avoid balance transfer because it could just make your situation worse.

If you think you might want to look into credit cards that offer a 0% introductory APR for balance transfers, you can shop over 150 different cards at our credit card marketplace at The Yukon Project. You will be able to see the latest offers, terms and conditions, and rewards. So, you can see if any of them would help you achieve your financial goals.

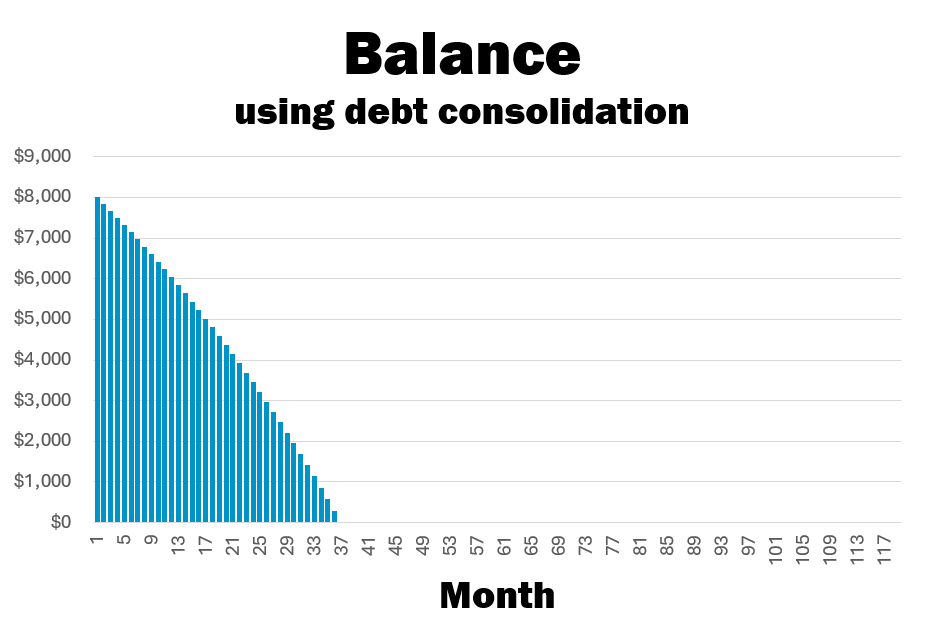

Debt Consolidation

Now let’s look at what happens when you consolidate your credit card balances into an installment loan. The key to debt consolidation is to increase your payment consistency and pay less in overall interest. The idea here is getting a personal loan that you use to pay off all your credit card balances. Aren’t you just trading one debt for another? Yes, but you are trading debt with variable payments for one with fixed payments. You are also getting a lower overall interest rate…because if you can’t lower your interest rate by at least 2-3 percentage points, you shouldn’t consolidate.

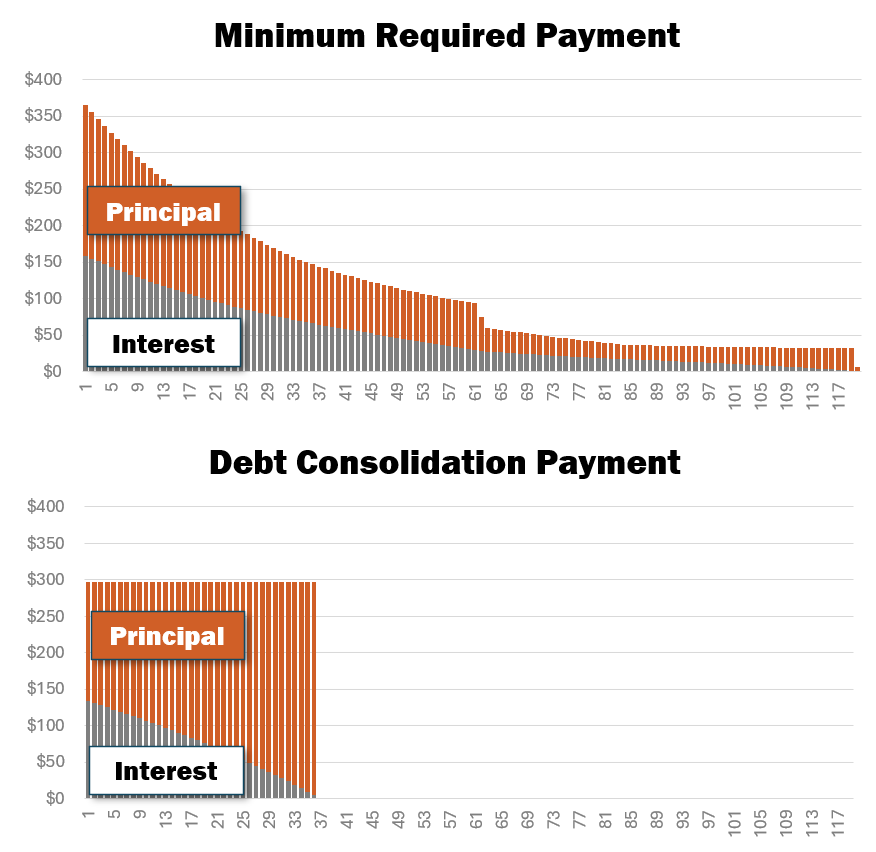

Here’s how debt consolidation looks. You can see that you can get out of debt in exactly 36 months, or three years.

Why does it work? Well, to put it bluntly, it forces consistent principal payments. This is what your monthly minimum payment is over time. This is what your monthly payment would be under debt consolidation.

If we deconstruct the payment, you can better see what is going on. The top graph is your monthly minimum payment split between the interest you pay and the principal you pay. The bottom graph splits interest and principal for the debt consolidation. You can see that over time, debt consolidation accelerates the amount of money that is going toward principal.

Debt consolidation compares pretty well with the other strategies we’ve looked at. The real value in debt consolidation is that it forces the payments. If you need that structural support, debt consolidation is a great failsafe method of paying off debt. If you can commit to yourself to make the extra payments as well–like you would under snowball or avalanche, you can see that you can get out in a similar speed as the other methods.

But, debt consolidation also has its risks. The biggest risk of debt consolidation is that you will run up your credit card balances again. If you do that, you will end up in worse shape than you were before.

If you want to check what kind of rate you could get on a debt consolidation loan, go to our marketplace page at The Yukon Project. You can apply directly to any one of our featured lenders. Behind the scenes, we will check your rate with up to 40 other lenders. Our partners use a soft credit check, so applying won’t hurt your credit score. We will show you all of your approved offers so you can pick the loan that works best for you.

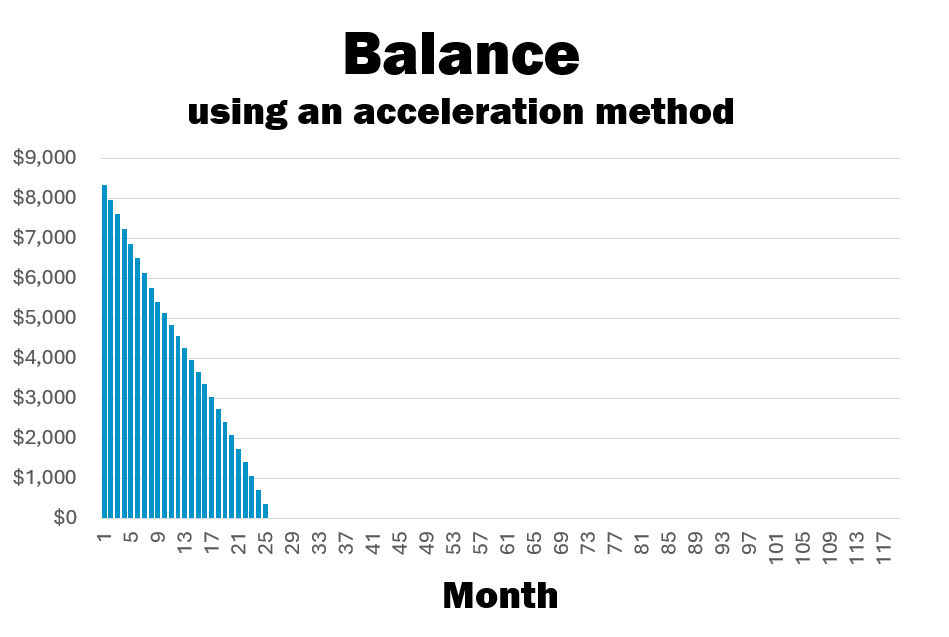

Acceleration

Now, I am going to show you how you can combine some of these techniques to pay off your debt in 25 months. Two years! This strategy actually combines three of the methods we have discussed today. First, we are going to be aggressive about your payment. In this scenario, you lock in the minimum payment you are making on your credit cards. This is the payment you will make from the beginning until the debt is paid off.

Second, we are going to get a new credit card that offers 0% APR for balance transfers. So, for eight months, every dime you pay will be going to principal. None of it will go towards interest. On the ninth month we will switch to our third method: you will get a debt consolidation loan for the remaining balance. The loan term will be for three years, but that doesn’t matter. You won’t have a prepayment penalty. Even though the monthly payment for the installment loan would be much lower, just continue paying what you have been paying. Doing that, you will have paid off the loan in the 25th month having paid a grand total of $801 in interest.

This combination leverages what we learned from the power of extra principal payments, the benefit of not paying interest from balance transfer, and consistency from debt consolidation. If you are making your payments right now, this strategy can work for you to help you get out of debt in two years.

Summary

So, there you have it. A comparison of eight different ways to pay off your credit card debt. It can take ten years or two years to pay off. It can cost you $5,000 or $800 in interest. The better you understand these strategies, the more you can use them to your advantage. If you have any questions about any of these methods, leave a comment below and we will try and get it answered. If you found this information helpful, like this video and subscribe to our channel. It really helps us out. Thanks for watching.

Stop paying the high interest rates from carrying a monthly balance on your credit card! Whether you need a small amount or $100,000 we have options for you!

Soft Credit Pull, Up To 40 Lenders at Once, See what you’re approved for!