Top things to know about credit inquiries:

- A credit inquiry is a record of the credit bureau disbursing your credit report

- Hard credit inquiries are generated when you apply for credit. All other inquiries are soft inquiries.

- Hard credit inquiries have no impact on your after one year. Soft inquiries never impact your score.

What is a credit inquiry?

A “credit inquiry” is the a record of when your credit report was accessed. It includes three key pieces of information:

- Who accessed your credit report

- When they accessed your credit report, and

- Why they accessed your credit report.

Under the FCRA there are detailed restrictions called permissible purposes that restrict access to your credit report. Therefore, it is imperative that credit bureaus keep detailed records of this access.

Keep track

You should keep track of any times that you apply for new credit. This will allow you to make sure that any inquiries are valid. This is a good way to help prevent identity theft.

What is a hard credit inquiry?

A hard inquiry is when your credit report is pulled for the purpose of obtaining new credit. That means a hard inquiry is only put on your credit report when you apply for new credit. However, some lenders will begin the application process with a soft inquiry. This means they review your credit to see if you meet their credit criteria. If so, they can give you a pre-approval with approximate terms for the credit offered.

What is a soft credit inquiry?

A soft inquiry is basically any credit inquiry that is not a hard inquiry. There are a multitude of different reasons for these to be on your credit report. Here are a some of the most common that you may have:

- Pre-approval in the application process for new credit

- Pre-approval through a pre-screening process (the credit offers in the mail)

- Checking your credit report (i.e. Credit Karma or annualcreditreport.com)

- Account management review by a current lender (most banks and creditors do it)

- Pre-employment credit review

- Insurance applications

How do hard credit inquiries impact my credit score

First of all, only hard credit inquiries impact your FICO score. Soft inquiries are never seen as part of the credit review process. The impact of hard inquiries is dependent on the number of inquiries and the time since each inquiry was made.

Although inquiries remain on your credit report for 2 years, they only impact your FICO score for one year. But even more importantly, if you don’t have any inquiries for three to six months, inquiries typically won’t impact your score more than a few points.

How many points does your FICO score go down for an hard credit inquiry?

If you only have one or two within the last few months, then hard credit inquiries will have minimal impact, think 5 to 10 points on your score. That impact should dissipate within a month or two.

Do multiple inquiries count as one?

If you are shopping around for the best options, you are likely to have several hard credit nquiries on your credit report in a short amount of time. Multiple hard credit inquiries that occur within a short time will not negatively impact your credit score any more than a single one will. If, on the other hand, you have hard inquiries over several months, those will impact your score more significantly than if they all took place in a short time period.

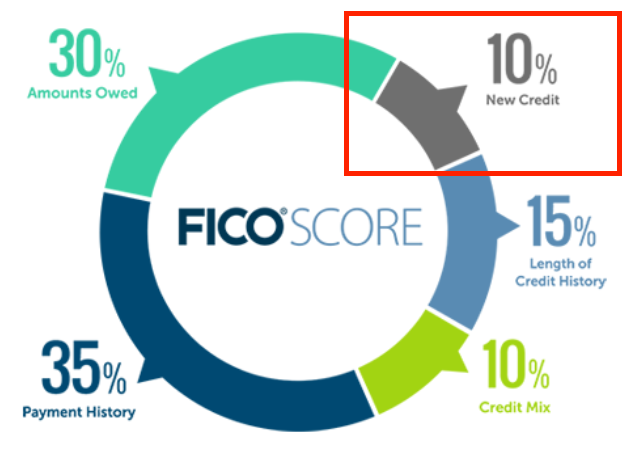

Do inquiries account for 10% of my FICO score?

Credit score articles and videos often say that inquiries account for 10% of your credit score. This is a misquote. The factor that accounts for 10% of your score is “New Credit,” which includes hard credit inquiries, but also includes new accounts. Inquiries are the lesser part of this factor.

Why does your credit score go down when you open a new credit account?

New credit accounts on your credit report indicate credit risk. Having accounts less than a year old, lowers your credit score. The newer the account, the more negative it is. And the more new accounts you have, the worse the negative impact will be. This is because newer accounts are the ones that most often default.

By simply letting your inquiries and new accounts age while making all of your payments on-time every month, you will see credit score improvement! It’s really that simple, time and on-time payments are all you need!