In this article

Buying a new car is a stressful process. There are so many things to consider. What kind of car should I buy? What can I afford? Am I getting a good deal? How can I get financing? Is the dealer tricking me?

Below are the 4 steps to follow to make sure you pay as little as possible for your next car! That means getting a good price on the car and the very best loan you can!

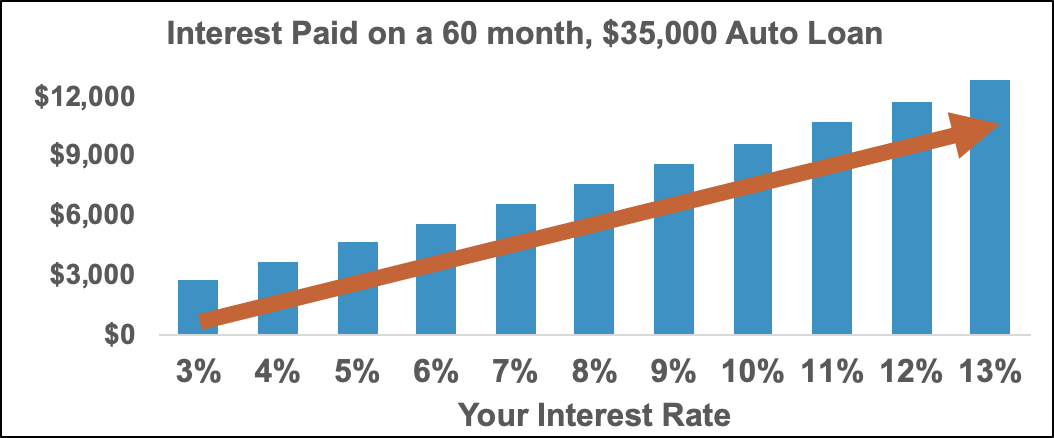

Your interest rate could cost you thousands!

Let’s start with the obvious. The interest rate you get makes a huge difference in your monthly payment and could mean the difference of thousands of dollars in the total cost of buying a new car.

With great credit you may be able to finance with rates as low as 4%! Even with fair credit, you can get an interest rate of 9%. But it’s up to you to make sure you get the best rate possible, because not doing so could cost you thousands!

Here’s the simple math. The average car cost $35,000 and the most common car loan term is a 60 month loan. Under these terms, every 1% increase in your interest rate will cost you an extra $1,000 over the life of your loan!

Steps to getting the BEST interest rate when buying a new car

- Know your credit score, and if possible improve it before buying

- Get pre-approved from at least one lender before visiting a dealership

- Negotiate the PRICE of the car first, without reference to financing

- Secure the best financing you can!

Know and improve your credit score

The first step to getting the best interest rate on your car is to know your credit score. This will help you understand what kind of credit you qualify for. Here is a good guideline to use. More importantly, it will let you know if you need to take a step back and work on your credit first.

Later in the article we will address how to improve your credit but here’s a quick look at if you need to improve your credit.

Credit score improvement needed by credit score

Credit scores below 600: You need to work on your credit first. Scores below 600 will mean very few lenders will approve you. If they do, the loan amount may not be what you need and the interest rate will be very high, possibly 15% or more!

Credit scores between 600 and 640: Some improvement is needed. There’s a good chance of you getting approved with this credit score. The interest rate will be high.

Credit scores between 640 and 680: Improving your credit score could save you thousands, but you will likely be approved and should be able to get a rate below 10%.

Credit scores between 680 and 720: Improving your credit score can save you thousands. You will almost certainly be approved. However, your rate likely won’t be the best rate available.

Credit scores between 720 and 760: You may qualify for the best rates possible, or you may be just short. Go ahead and start the pre-qualification process if you want to see what’s available. Some improvement in your score could help though.

Credit scores between 760 and 800: You very likely already qualify for the best rates available! Usually you are considered “super-prime” with a credit score in this bucket. Credit score improvement really isn’t likely to be needed.

Credit score above 800: You’re considered super-prime credit! You will almost certainly have access to the very best rates available from any lender or dealer.

Get pre-approved for an auto loan BEFORE visiting a car dealership

You should get pre-approved with at least one lender before going to any car dealership. A great place to start is your current bank or credit union. You can also shop online for a pre-approval if you prefer.

When looking for a pre-qualification, make sure the inquiry will be a soft-inquiry on your credit. That means it won’t impact your credit score. If it’s a hard inquiry, you might want to pass and go somewhere else.

Depending on where you’re getting pre-approved, you may be asked for details about the car you want. They may do a blanket pre-qualification for a set loan amount. Don’t worry about answering this question perfectly. Answer with your best estimate, you can update the information later once you have the details of the car you want to purchase. Note that the final loan you get will depend on the car you end up purchasing.

Getting pre-approved gives you a baseline for your negotiations with the dealer. It’s quite likely that you will decide to use a dealership loan, but having this loan gives you a good idea of the rate you should get. And if the dealer can’t beat it, you can certainly use it!

Negotiate the car price first

Once you’ve gotten your pre-approval, you’re ready to go car shopping. But the most important thing is to focus on the price of the car first! If the salesman asks you “What kind of payment are you looking for,” kindly respond that you are looking for the best price possible on the car! NEVER answer that question! You give away way too much information when you do.

This way, you are first securing the best possible price of the car. When you give them a payment, they have a few tricks that they might use to pressure your purchase or make the cost higher than needed.

- They will get the monthly cost in your range and pressure the purchase because they “gave you what you were looking for.”

- They may extend the term of the loan and offer a suboptimal rate as long as it falls into your range.

- They may withhold some discounts on the car if they are not needed to meet the monthly price.

By locking in the price of the car, you can then focus on getting the best rate and term that your credit will allow.

Secure your financing

With the price of your car locked in, you can then work on getting the best rate possible. Hopefully one that is even lower than your pre-approval rate. Sometimes dealers have incentive programs that allow you to get special rates. These rates cannot be matched by outside lenders. But even if they don’t have that, they do usually have multiple lenders at their disposal and can often get you financing. That being said, if they are not offering you some special incentive rate program then they may not be trying to get you the best loan.

Why should I get pre-approved with a bank or credit union before going to a car dealer?

Car dealers are under no obligation to offer you the best loan offer they get from you. And they probably won’t. They are going to offer you the loan that pays them the most. Because they receive a commission on the loan that you choose.

One thing very few people know about when getting a car loan from a dealer is what’s called the “reserve”. Legally, they can add up to 2% to the interest rate that the bank offered you. So if Bank XYZ tells the lender they can give you a 5% interest rate on your car. Then the salesman could offer you up to 7% on the loan. And yes, if they get you to take 7% then they make more money than if they offered you 5%.

Why negotiate the price of the car first

When you buy and finance a car, you are actually making 2 major financial decisions in one. First, the price of the car and second, the terms of your loan. Car dealers will combine these and then manipulate them to make it seem like a good deal. Pro-tip for car buying. Negotiate the car price first. Then the financing.

But you should tell them you are interested in financing, even if you have cash. Contrary to popular belief, cash buyers don’t always get the best price on the car. That’s because the dealer makes money on the financing too. So, lock down the price of the car, including all add-ons etc. Then talk about financing.

New car buying warning and a tip

You are at a disadvantage when it comes to car negotiations. Even the most experienced person probably buys 5 cars or fewer in the last 10 years. The dealer, and their team of salespeople, do it several times every day. So, take your time. If you can, negotiate with multiple car dealers to get a better price (they hate this, precisely because it takes away their advantage). Most importantly, be willing to walk away from them.

How long will it take to improve my credit and reduce my interest rate on my car loan?

First, let’s talk about timing. Credit reporting, and therefore credit scores, runs on a delay. This is because the information is not shared to credit bureaus daily. You lenders will be sending your information to the credit bureaus no more than once a month. So, you should expect that any changes you make today could take 30 to 40 days to impact your credit score. When buying a new car, you’ll need to plan accordingly!

How can I improve my credit to reduce my new car loan interest rate?

To improve your credit, I would stick to my basic steps. 1) make sure your credit report is accurate. 2) make sure all of your accounts are in good standing i.e. paid on time. 3) create a credit foundation of at least 3 open, active accounts in good standing.

In the short term, opening new accounts won’t help you. Because they take a while to become a positive on your score. In the short term 60 to 90 days, the best improvement in your credit score will be 1) removing any collections and 2) reducing your debts, especially credit card debt. 3) lowering your credit card utilization rate.

I put lowering your utilization rate separately because you could get a credit line increase or become an authorized user on someone else’s card, both of which can lower the rate without lowering your debts.

If I can get 0% financing for my new car, should I put anything down?

This is a personal preference question. But note there’s usually the catch is this. You can choose a discount on the price of the car or 0% financing, but not both. So you pay more for the car to get the 0% APR. Usually the 0% financing is mathematically a better deal, but some people would prefer not to have debt. There’s not a right or wrong choice here, choose what makes the most sense for your financial life.

Should I take a 72 months loan or a 60 month loan for my car?

There are 2 factors missing from this question that are imperative to making a good choice when buying a new car. First, what is the interest rate on the 2 loans, and second, does either have a prepayment penalty. Very few lenders charge a pre-payment penalty but don’t assume there isn’t one. If neither has And if the monthly payment on the 72 month loan is a lot lower, then the interest rates are likely similar. In that instance, take the 72 month loan but make monthly payments equal to or greater than the 60 month loan would require. This way you have the flexibility to pay less if needed but put yourself on the path to 60 month payoff if you can afford the higher payment without issue.